Gold is doing 'spectacular job' but price drop to $1,800 not ruled out, here's why

Gold surprised this week with its resilience and steadiness after an oversized 75-basis-point hike from the Federal Reserve and massive volatility across many markets. But analysts don't see a major rally developing in gold in the short-term, and they are not even ruling out a move back to $1,800.

The precious metal's reaction to the Fed's decision to raise rates by 75 basis points — the biggest increase since 1994 — has been very encouraging. Fed Chair Jerome Powell also signaled that another 75bps is possible in July, adding that the so-called 'softish landing' will now depend more o external factors like commodity prices.

After digesting the information, the stock market saw a sharp drop, while gold rallied around $40 on Thursday. However, the rally was short-lived as August Comex gold futures retreated to 1,841.70 an ounce Friday, down 0.44% on the day.

"Gold's current relative stellar performance is surprising, as it usually tracks the Fed's policy rates and real interest rates intently," TD Securities global head of commodity strategy Bart Melek. "And, the market hiked its year-end Fed Funds expectation from 2.7% in mid-May to 3.6% now. At the same time, the 10-year real rate, which is the usual driver, jumped well over 50bps from a month earlier to 0.69% and some 180 bps higher from the start of the year."

The performance of gold versus that of other markets stands out, said Gainesville Coins precious metals expert Everett Millman. "Other markets you look at, even some safe havens like the U.S. dollar, have been remarkably volatile. Gold has had relatively low volatility. It is a sign of strength and gold doing its job — holding steady even amid turmoil across other assets," Millman told Kitco News.

Year-to-date, gold is largely flat, up 0.5%. Yet, Millman pointed out that this resilience does not mean a rally is just around the corner.

"We've seen gold rally nice and then pull back. I expect that to continue up until the next Fed meeting in July. Gold will be range-bound and stuck trading sideways until we find out whether the Fed will go through with another large rate hike," Millman said. "Rate hikes are supposed to be bad for gold. But when inflation is this high, it will take many rate hikes for the Fed to get to where the real rate of interest rate is neutral. And that is what gold cares about. Maybe next year, they will get there."

What's next for crypto after 'perfect storm' crashes prices? Ethereum's market cap is 'orders of magnitude higher' than Bitcoin — Messari

Throughout the summer, Millman sees gold between $1,800 and $1,900, with $1,840 flipping from support to resistance and vice versa.

He added that even though inflation remains one of the primary drivers for gold, growing recession risk could encourage some additional gold-buying if investors continue to fear losses in other assets.

Gold has been doing "a spectacular job," described Melek. But that doesn't mean the precious metal doesn't correct here and returns back towards $1,800. "It won't be a rout but a modest correction," he said.

The thinking behind Melek's projection is a persistent Fed, which won't give up aggressive rate hikes at the first sign of economic trouble. "My suspicion is that the Fed won't change its mind any time soon," he said. "It is very likely there will be many more aggressive hikes in the face of strong inflationary forces, which will likely send gold back to the May lows."

And that means a return to the $1,824-$1,808 range in the near term. "Still think we can go below $1,800 by the end of the year. It is too early to say that the Fed will flake at the first sign of trouble. Could be in a situation where growth starts to slow, but we won't see a significant move in inflation until September or October."

Data to watch next week

Out of all the macro data on the docket for next week, housing will be a vital element to keep a close eye on. The key thing to watch is the impact of the Fed's higher rates on the economy, including the housing market, said ING chief international economist James Knightley.

"With the Federal Reserve signaling it has a strong stomach for the fight against inflation, we have to expect further significant interest rate hikes in coming months. But by going harder and faster into restrictive territory, there is a greater risk of a hard landing and a potential recession," Knightley said in a note Friday. "The housing market is particularly vulnerable given prices are up nearly 40% nationally since the start of the pandemic due to stimulus-fuelled demand vastly outstripping the limited supply of properties for sale."

Another event to monitor will be Powell's testimony before the Senate Banking, Housing, and Urban Affairs Committee on Wednesday and the House Financial Services Committee on Thursday.

Tuesday: U.S. existing home sales (May)

Wednesday: Fed Chair Powell testifies

Thursday: Fed Chair Powell testifies, U.S. jobless claims, U.S. manufacturing PMI

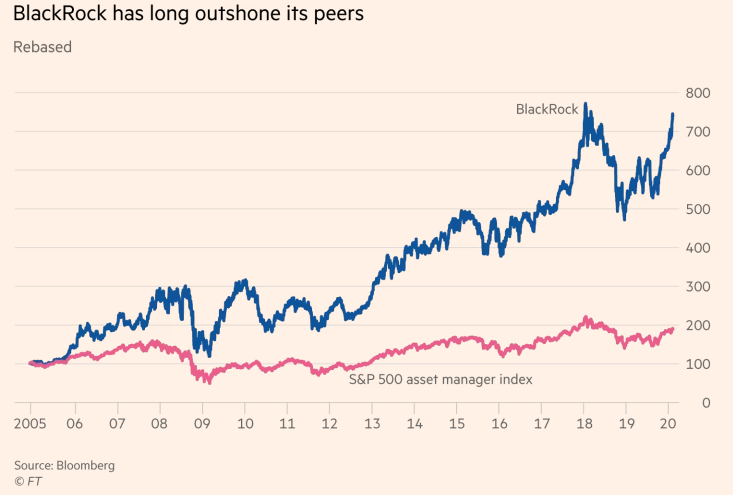

BlackRock – Shadow Government?

Is It Too Big To Fail? Or Has It Now Got Too Big To Control?

There is a company out there that has more funds running through its systems than the entire GDP of the USA. A company that can and has used its clout to effect “societal change” whether we like it or not. A company with a direct connection with powerful politicians in the world has recently come front and center as it has started exploring investments in the crypto space and venturing into governance territory that will impact worldwide.

The BlackRock Behemoth

BlackRock is the world’s largest asset manager, and while many may have heard of it, you may be surprised just how much control it has over the financial markets. A control is afforded to it through leveraging our money, so there’s a strong chance that you and your money are connected with it somehow. It is a company that has its fingers in many pies, with over $10 trillion in assets under management.

They are also one of the most secretive companies in the world of finance. Trading and commodities are two areas of BlackRock’s business that have come under scrutiny from government regulators in recent years.

The Commodity Futures Trading Commission (CFTC) has claimed that the process of trading commodities futures is not transparent and is likely being abused by large investment firms like BlackRock. One of the most controversial aspects of BlackRock’s business is the way they have been operating their so-called dark pools.

Blackrock’s political connections are extensive. Over the past couple of years, there has been growing concern about how much control large corporations like Blackrock exert over American politics and economic policymaking.

Although they claim to be a non-political organization whose only interest is maximizing shareholder value, it is clear that many large corporations like Blackrock do wield significant influence over how our government works and what kinds of policies it enacts into law.

BlackRock is a New York City-based company founded in 1988 by Laurence [Larry] Fink and Ralph Schlosstein. Starting as a Bond Asset manager, it quickly grew into a financial services company that provides investment management, risk management, and fiduciary financial services to a wide variety of clients ranging from Central Banks to pension funds and individual investors.

In 1999, BlackRock became a publicly-traded company and continued its rapid expansion in the asset management sector. In 2006, the firm acquired Merrill Lynch's Asset Management business, which rapidly expanded its offerings in the equities sector. This was further compounded by the purchase of Barclay’s iShares in 2009. At $13.5 billion, this was one of the biggest deals in Asset Management history.

As a result, BlackRock quickly morphed from being a bond asset management company to an Index Fund provider. Index Funds, sometimes called Exchange Traded Funds, are collective investment vehicles that track the performance of a particular index or basket of Securities. They're hugely popular, not only because they're easy to invest in but also because they incur lower fees than more active investment management firms.

These benefits have also made index funds extremely attractive for more passive institutional investors, the most common being pension funds. Trillions of dollars are invested on our behalf and find their way into index funds of some sort. So there’s a strong possibility our money has been invested through BlackRock somehow. Either that or it's being invested by another index provider thanks to BlackRock’s technology.

The point is that BlackRock is a behemoth that invests on behalf of hundreds of millions of people, and what that means is it has an interest in nearly every company you can think of. Since BlackRock must invest funds to track indexes or other investing themes, it must invest in the underlying assets. If these funds track an equity index, BlackRock must take a stake in the underlying company, so BlackRock is often one of the largest shareholders of a company's outstanding shares.

These companies include some of the biggest Wall Street banks, like Goldman Sachs, JP Morgan, Bank of America, and Citibank. Essentially, BlackRock is one of the top three shareholders in the banks that keep the financial markets running.

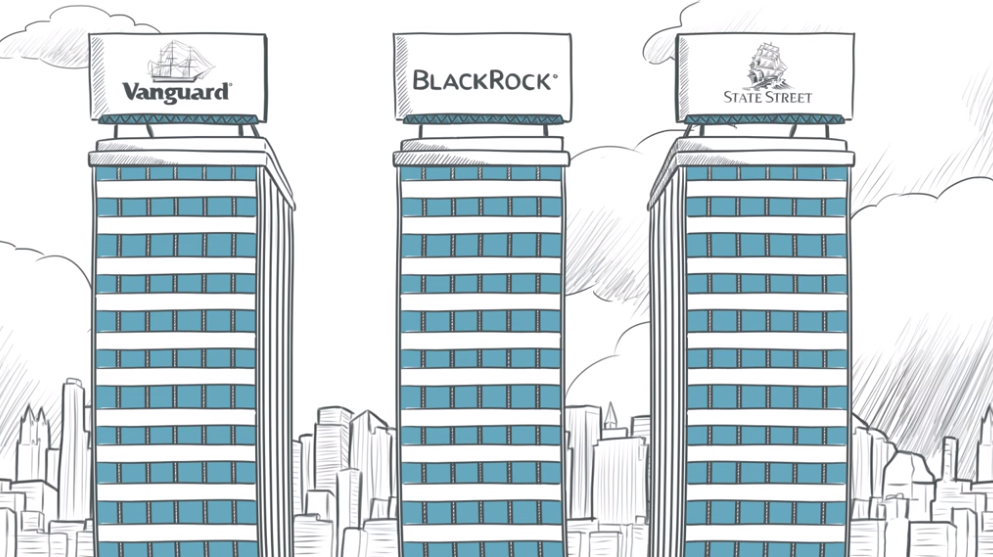

BlackRock is also vested in the media with Comcast, Viacom, et al. Also, social media and tech companies with large stakes in Google, Apple, and Twitter. They even have stakes in the food industry with Mcdonald's, Chipotle, et al. Along with State Street and Vanguard, BlackRock forms a trio of the largest shareholders in the vast majority of publicly-traded companies in America.

For example, according to a recently published paper by Corpnet, these prominent three asset managers are the largest shareholders for over 90% of all companies in the S&P 500. In fact, in the broader collection of all outstanding publicly traded companies, 40% of them have these three as their most significant shareholders. And it’s not just America; it holds considerable positions in companies in Europe as well.

A Slice Of The Real Estate Pie And Now Crypto

BlackRock has its eyes on cryptocurrency with BlackRock CEO, Larry Fink saying the firm is studying the crypto sector broadly, including assets, stablecoins, permissioned blockchains, and “tokenization,” where it perceives a benefit to its customers. We are increasingly seeing interest from our clients, he said.

BlackRock is an investor in a $400 million fundraising round for Circle Internet Financial, the crypto-focused company that manages the stablecoin USD Coin. During a conference call in April 2022, Larry Fink said BlackRock has been working with Circle over the past year as a manager of some of Circle’s cash reserves. He said he expects BlackRock eventually to be the primary manager of those reserves. We look forward to expanding our relationship, he said.

You might also be surprised to learn that asset managers like BlackRock have been competing with you regarding residential real estate. Last year, large institutional investors bought up entire property units to diversify their holdings. Just imagine, large asset managers could potentially be using your pension money to outbid you on a home. Despite how crazy all this sounds, it’s just the tip of the iceberg.

ALADDIN – BlackRock’s Genie Of Growth And Control

BlackRock has not only made a name for itself through its index funds, but it's also developed an institutional investing platform that is the backbone of the asset management system. The “central nervous system” is relied upon by nearly every billion-dollar capital allocator. It’s called Aladdin, an acronym for Asset, Liability, And Debt, Derivative Investment Network.

Since Aladdin’s humble beginnings as a time-saving system that BlackRock could use to report on bond positions automatically, it has grown over the years to become the operating system for the company that inhabits multiple data centers and is maintained by a group of between 1,500 and 2,000 people.

Aladdin is so integral to BlackRock’s internal risk management systems that around 13,000 BlackRock employees use it worldwide. Aladdin also became so sophisticated that BlackRock saw an opportunity to start making money from competing asset managers, institutional investors, and corporates by making the platform available to them. It would also allow these investors to manage their portfolios and model the inherent risk.

The list of companies that use Aladdin is vast, with over 240 external clients currently relying on the platform. Companies like Google, Apple, and Microsoft use it for their corporate treasury management. The $1.5 trillion Japanese government pension fund is also a client, as well as State Street and Vanguard.

So, in reality, BlackRock’s biggest competitors are effectively paying to use BlackRock's systems and, in the process, giving BlackRock access to reams of data about their portfolios. This data further helps BlackRock refine Aladdin and better model risk. Needless to say, because all these portfolios are linked, it certainly gives BlackRock the edge with Aladdin as a critical component in the global management of assets.

In 2020, an estimated $21.6 trillion sat on the platform, which is higher than the entire GDP of the United States at that time. Another comparison is if you were to empty the bank account of every one of the 7.6 billion people in the world, every single bill and coin, and place them all in a pile, it would be worth around $5 trillion.

So, this means that Aladdin has grown into a system that is responsible, directly or indirectly, for over four times the value of all the money in the world. Aladdin doesn’t make investment decisions, but its risk models inform the investment decisions of all who use it.

There have been many who have questioned whether this system poses a systemic risk to the market. For example, given how many managers rely on its analytics and modeling, does this create complacency and reliance that could give a false sense of security? What happens if there are inaccurate or erroneous readings? It's only a computer model, after all.

A UK regulator, the Financial Conduct Authority, reported that the failure of an extensive portfolio and risk system like Aladdin could cause serious consumer harm or even damage market integrity.

Jon Little, former head of BNY Mellon's international asset management business, told the Financial Times,

“The industry is becoming reliant on a small number of players such as Aladdin, yet regulators seem to be reluctant to regulate or intervene to supervise these key service providers directly.”

This video sums up the level of involvement BlackRock has with their technology, Aladdin has and looks somewhat like a terrifying science-fiction scenario, but it is happening today.

BlackRock’s Helping Hand

Did you know that BlackRock was instrumental in the bailouts and deals in 2008’s GFC? It was a key adviser to other big banks and the government itself. So BlackRock is not only a massive asset manager that controls one of the world’s most powerful computers, but it also offers advisory services.

It’s called the Financial Markets Advisory or FMA. It was born from the financial crisis as these big banks, along with the US Treasury and Federal Reserve Bank of New York, turned to Larry Fink of BlackRock for help and counsel on their predicament.

Through an array of government contracts, BlackRock effectively became the leading manager of Washington’s bailout of Wall Street. The firm oversaw the $130 billion of toxic assets that the U.S. government took on as part of the Bear Stearns sale and the rescue of A.I.G.

It also monitored Fannie Mae's and Freddie Mac's balance sheets, which amount to some $5 trillion. It provided daily risk evaluations to the New York Fed on the $1.2 trillion worth of mortgage-backed securities it had purchased to jump-start the country’s housing market.

Eleven years after the financial crisis, we had another emergency, the pandemic, which brought on a level of spending that was many multiples larger. The FED embarked on an unprecedented bond-buying program and monetary stimulus. These were trillions upon trillions of dollars that are used to buy back not only treasury securities but, more risky, corporate bonds and mortgage-backed securities.

And, of course, they needed the advice of someone who knew about these types of securities. Thankfully, they had the industry experts such as Larry Fink on speed dial. It was later disclosed that BlackRock was central to the pandemic response. According to this New York Times article, Larry Fink was in constant contact with Jerome Powell and Stephen Minuchin in the days before and after the FED's stimulus program announcement.

According to a contract posted in March 2020, the FED hired BlackRock to help with the corporate bond purchase program. Although there was much more transparency about the terms of the deal compared to its work back in 2008, it meant that BlackRock was instrumental in that bond-buying program.

It again shows how reliant these officials have become on this behemoth of Wall Street. So it's clear that BlackRock has political influence or, at the very least, is aligned with some really powerful people. But perhaps more concerning about the firm is its power and intention to exert over corporate board rooms.

BlackRock’s Role And Goal Posts Have Shifted

As mentioned above, BlackRock and the top three asset managers generally are the largest shareholders in hundreds of Fortune 500 companies. What this means is that not only do they own the shares, but they also get board representation. These corporate boards are designed to help advise on company strategies, and board members can have much more say in a company’s strategic objectives.

Given that BlackRock invests on behalf of clients, it is considered a passive investor, meaning it's merely tasked with allocating capital and voting in the best interest of shareholders. Up until a few years ago, that's precisely what it did. However, in 2018, it all changed because, at this time, Larry Fink wrote a letter to the CEOs of some of America's largest public companies. This was the first salute in his pitch to better contribute to society,

“Society is demanding the companies, both public and private serve a social purpose. To prosper over time, every company must not only deliver financial performance but also show how it makes a positive contribution to society.”

This was a novel idea at the time but has since shaped the mood around investing based on ESG or Environmental Social and Governance principles. The primary modus operandi behind this investing methodology is that companies should not only be graded on their bottom line but also on how they impact society.

This letter was a big deal. You had one of the most powerful investors on Wall Street saying that it would be using ESG criteria to grade companies, everything from their climate change records to diversity on their boards. Some wondered whether BlackRock really would carry out these plans for a more activist role; any doubts on the matter were laid to rest with some controversial shareholder votes.

For example, last year, BlackRock disclosed that as Exxon Mobil's second-largest shareholder, it was backing board changes proposed by an activist hedge fund. The fund in question was Engine No 1, and it's been trying to get Exxon Mobil to move faster in reducing its carbon footprint. The activist investor only held about $50 million in stock but had proposed some board members who Exxon claimed didn't possess the requisite skills to serve on the board.

As mentioned in this WSJ report, BlackRock also backed similar initiatives by voting against a board director of an Australian oil and natural gas producer called Woodside Petroleum. The reason for the vote was that the company was not outlining targets for emission reductions to its customers. So the world’s largest asset manager is showing it is more willing to use its heft to influence the policies of the companies it invests in.

Rich Field, a partner at the law firm King & Spalding, who focuses on corporate governance issues, said,

“BlackRock has strongly signaled that quiet diplomacy is not the only tool in its toolbox. We expect more votes for shareholder proposals and against directors in this and future years.”

Since 2020, BlackRock has stepped up pressure on more companies by publishing criticism with online bulletins about key votes. Some executives worry they could face lawsuits for publicizing details on labor or climate plans in areas where global disclosure standards don’t yet exist.

There are so many boards that BlackRock sits on that it could be hard to apply proper due diligence to these ESG votes. Some have complained BlackRock’s recent votes have come without warning or an adequate rationale. Ali Saribas, a partner at shareholder advisory firm SquareWell Partners, said,

“BlackRock’s approach will fuel a rising frustration among companies that believe BlackRock’s stewardship team will most likely apply a tick-the-box approach given the sheer volume of companies they passively own.”

Jessica Strine, CEO at advisory firm Sustainable Governance Partners, says,

“It would be very hard for a passive fund manager to support a shareholder proposal that addresses systemic risks but wades too far into dictating strategy.”

Investors propelled ESG funds to new heights in 2020, and federal agencies are watching. WSJ explains why regulators have ethical and sustainable investment funds under review. Photo Illustration: Alex Kuzoian

Has BlackRock Gone Too Far?

Some may think this is good news for a better future. Still, one of the biggest problems with this approach is that it assumes that meeting these ESG criteria could be complementary to the shareholder returns objectives.

However, this is often not the case because meeting these criteria may come at the expense of potential company performance and long-term shareholder returns. For example, in the case of the Exxon proposal, unless these standards are applied to all competing companies in the field, you are hampering some to the advantage of others.

Many oil and gas companies are private or listed elsewhere, companies that don't have BlackRock as a shareholder and hence don't have to worry about meeting the same standards. They can compete as much as the law allows them to, and sometimes to the detriment of Exxon. This could lead to a fall in the value of Exxon shares and the company as a whole.

Now the same principles can, of course, be applied to the S and G angles of the ESG strategy too. Then, of course, you have the administrative burden and the unpredictable way this ESG mandate is managed.

The approach that BlackRock wants to take could hamper the efficient performance of a company's board and corporate strategy, which is unsuitable for that long-term shareholder value. Beyond the additional burdens that this could place on companies, you have the question of whether a company like BlackRock should have such a significant say in how society is shaped.

The Silenced Majority

Have all the stakeholders, the millions of us who have pension funds and invest in ETFs, been asked how we feel about these proposals? Are stakeholders polled on each one of these proposals? And how do we know there's no broader political agenda that could seep in should the winds of public opinion shift. Does this create a precedent for other large companies to follow suit? These are all relevant questions that need to be answered. It is, after all, good governance.

Many of us know BlackRock is a powerful company but to realize how far that power extends is an eye-opener, to say the least. As the world's largest asset manager, it manages an ocean of capital that gives it immense control over the financial system.

Given that it's the owner and operator of one of the largest and most crucial asset management platforms, many would argue that it's too big to fail, but more to the point, it's now too big to control. That's because BlackRock seems to be taking on a new mission beyond mere capital allocation.

The firm is looking to use its ESG mandate to shape the way that corporate America is run. It's also not as if politicians can really do much about it. Given BlackRock's connections with all of these higher-ups, it is more likely to call the shots than the other way around.

Of course, the mandate and goals of BlackRock may be benevolent and sincere, but you have to question how this power could be used in the future should it fall into the hands of someone who would use it for more than just ESG benchmarks? Money is power, after all, and given that BlackRock controls so much money, it has absolute power. And as the saying goes, absolute power corrupts, absolutely.

by Joyce Chen, a writer, editor, and community builder based in Seattle, Washington

Celeb dads, they’re just like us!

Many of the biggest names in music, tech, politics, sports, and Hollywood also happen to be just good ole “Dad” to their kids. These famous fathers have found ways to stay connected to their little (and not-so-little) ones, and can’t help but extoll the wonders of seeing the world through their children’s eyes.

For some of them, fatherhood has meant learning how to slow down and appreciate the little things; for others, it’s required getting more intentional about their careers, so they can maximize time with their kids. But most celebrity dads agree that fatherhood has been humbling — a reminder that their most important job in life is to care for and help raise the next generation of changemakers. Or as Prince Harry put it, “Perhaps it’s the newfound clarity I have as a father, knowing that my son will always be watching what I do, mimicking my behavior, one day maybe even following in my footsteps.” Below, we’ve rounded up 15 other heartwarming quotes about fatherhood, from some of today’s biggest names.

[Parental love] is a different kind of love. It's very pure, it's unconditional, but they haven't earned it yet. They didn't do anything, they just exist and you love them completely, but it's not built on anything other than their existence. — John Legend

Being a father is the single greatest feeling on Earth. Not including those wonderful years I spent without a child, of course. — Ryan Reynolds

More than anything you have to make time to be with your children. It’s something I battle a lot because of my career, because as much as it’s nice to be busy and working, ultimately children don’t raise themselves. You’ve got to be there to help them and guide them through it. — Idris Elba

Love, respect, and hard work, honor, and discipline, all the stuff I learned [being a father]. [Zoë is] amazing, and she’s all the things that I would have hoped for. I’m [her] dad you know, but we’re friends. We’re very close. We talk about everything. We don’t hide things from each other. — Lenny Kravitz

[Becoming a dad] made me want to work harder and get focused and do the right things, so the right things could happen for me and my kids. — Mario Lopez

Men should always change diapers. It’s a very rewarding experience. It’s mentally cleansing. It’s like washing dishes, but imagine if the dishes were your kids, so you really love the dishes. — Chris Martin

I finally understand Game of Thrones. I think about how I would do anything for my daughter, and also my wife. [Fatherhood] gives me this clarity of thought around every decision I make, not just professionally, but personally, and everything else. It just feels really good. It's like a higher level of consciousness. — Alexis Ohanian (co-founder of Reddit, husband to Serena Williams)

The love I have for my wife is so intense, but nothing prepared me for the love I have for my kids. That feeling is overwhelming. The thought of them being in any trouble, any pain… I would do anything to avoid it. — Hugh Jackman

It's a full-on assembly line… They harmonize when they cry. When one cries, two cry, then three cry. Chain reaction is a real thing at our house. — Pharrell

Being present with your child, that’s the greatest gift that you can give to any child, your attention. — David Beckham

I worry about the future more. When you have something or someone in your life to give the future to, I think it focuses the mind more about what you're giving them. Are you happy that you've done all you can to leave it in a good state? — Prince William

I’ve been a parent for three weeks. What do I know? I don’t know anything, but it’s kind of part of the beauty of it, honestly. There are a lot of instincts, a lot of things that kind of kick in and switch on. It’s a beautiful experience. — Adam Levine (shortly after the 2016 birth of his twin daughters Dusty and Gio)

I thought I'd never be that annoying person [who shares pictures of his kids], but as soon as Winnie was born, I was showing iPhone snaps to a cab driver. — Jimmy Fallon

We pass on the values of empathy and kindness to our children by living them. We need to show our kids that you’re not strong by putting other people down — you’re strong by lifting them up. That’s our responsibility as fathers. — Barack Obama

My kids are my greatest piece of art. If I can pump them full of amazing stuff and surround them with beautiful art and music, then I’m going to live out my life watching them. They’re already way smarter and just way better than me. God, I love it. It’s beautiful. I want it to be the greatest thing I ever do: Make good humans. — Jason Momoa

New Opportunities Are Emerging For Citizens of The World.

Freedom and democracy may appear to be struggling to stay alive in America, but there may be a knock-out punch ready to be released. The evolution of the blockchain-enabled metaverse is going to enable the 'Citizens of the World' to gain their own Freedom by democratizing power and creating a new world with new rules, new players, and new opportunities. For 99.99% of us, the metaverse will improve our real-world lives through the democratization of power and opportunity.

Along with the major long-term trend of society towards decentralization and smaller-scale organizations, there are new opportunities developing to help 'Preparers' in the cryptocurrency sector. Businesses are beginning to issue their own Crypto Coins that can be traded on Cryptocoin Exchanges.

Markethive.com for example will be releasing its HiveCoin (HIV) in the coming weeks. It has tremendous upside potential that is outlined in a Video by Founder Tom Prendergast, "Entrepreneur Advantage…".

Not only that, if you go to their website and register as a FREE Member, you will be given 500 HiveCoins for "FREE" along with access to several Earning Opportunities and online tools to increase your HiveCoin balance.

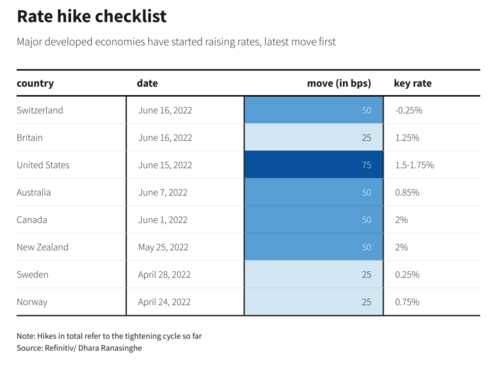

A tug-of-war takes gold lower, then higher, and finally lower on Friday

Gold traders experienced extreme price volatility beginning with a $70 drop on Monday and Tuesday, higher prices on Wednesday and Thursday, and a final price decline on Friday. This tug-of-war shifted market sentiment causing market participants to concentrate on either spiraling inflation or higher interest rates. The shift between these two opposing forces resulted in dramatic price increases and declines.

Last week’s CPI report which revealed that the current level of inflation is at 8.6% created bullish undertones moving the market higher during the middle of the week. However, the focus shifted to the Federal Reserve's revision of its forward guidance announcing a rate hike of 75 -basis points (3/4%) on Wednesday taking fed funds rates to 1.5% – 1.75%. This was the largest single rate hike since 2009.

Based on a weekly price decline in gold of approximately $40 the clear winner of this tug-of-war is the interest rate hike enacted by the Federal Reserve on Wednesday.

Wednesday’s rate hike was followed by rate hikes from other central banks. On Thursday with the Bank of England raising rates by 25 basis points, the SNB (Swiss National Bank) raised its interest rates by 50 basis points. This follows last week’s announcement by the ECB (European Central Bank) of a 25 basis point rate hike in July and a potential 50 basis point hike in September.

According to Bloomberg News, “June 2022 will certainly be a month to remember in central banking. Global monetary policy makers have laid out the most powerful tightening campaign since the 1980s, with a number of central banks embracing interest-rate increases of a size unimaginable at the start of the year.”

As of 5:10 PM EDT gold futures basis, the most active August contract is currently fixed at $1841.90 after factoring in today’s decline of eight dollars or 0.43%. Today’s price decline in gold was also the net result of dollar strength. The U.S. dollar gained just over 1% (1,01%) taking the dollar index to 104.46. The dollar also closed higher on the week.

Today’s price decline took gold just below its 200-day moving average which is currently fixed at $1843. Our technical studies indicate that current short-term support for gold occurs at $1830 which is the 61.8% Fibonacci retracement. Major support for gold occurs at $1765.50 which is based upon the 78% Fibonacci retracement. The data set used for this retracement begins at the lows and double bottom that occurred at $1680 up to the yearly high of $2078.

These studies also indicate that the first level of resistance occurs at $1860 which is based upon the highs of Thursday and Friday. Major resistance starts at $1878, the 50-day moving average, and $1889.70 which is based on the 100-day moving average.

Gold prices have fluctuated based on the primary focus of market participants. The tug-of-war between focusing on inflation levels or interest rate hikes will continue to be a primary force affecting gold prices through the remainder of this month.

Silver caught between an industrial metal and a monetary asset

Silver prices are on the move to the top of their current trading range, looking to test resistance around $22 an ounce. Although the precious metal is supported by long-term fundamentals, commodity analysts at BMO Capital Markets said that growing recessionary risks could weigh on prices in the near term.

While silver is considered a monetary metal, the analysts noted that its role as an industrial metal had been a dominant factor. They added that so far this year, silver has been trading as a risk-on asset, "which does not bode well for prices if economic headwinds mount."

They added that as recessionary pressure build, gold prices will continue to outperform silver.

The analysts noted that investors' preference for gold over silver can be seen in the paper market as demand for gold-backed exchange-traded products has outperformed silver-backed exchange-traded products.

"Despite gold-backed exchange-traded funds (ETFs) seeing net inflows of 225t year to date, owing to multi-decade high inflation, geopolitical tensions, and mounting recessionary fears, silver ETPs have seen net outflows of 269t since the start of the year," the analysts said.

Lukewarm investor interest in silver can also be seen in the physical market. The Canadian bank said that demand for silver bars and coins is expected to rise by 213 million ounces this year, down nearly 24% from last year. However, the analysts also noted that physical demand will remain well above the previous highs hit in 2015.

Looking past the paper and physical market, BMO analysts said that investors should keep an eye on the metal's industrial applications.

However, the analysts also said investors shouldn't ignore silver's long-term fundamental outlook.

"We expect to see silver's longer-term industrial uses, particularly related to the energy transition, to continue to help support near-term investor sentiment," the analysts said. "Industrial silver demand is undergoing its own transition. Industrial demand, including photography, is set to grow by 117Mozpa by 2030, compared to 2021 levels, that is equivalent to the total amount of primary silver expected to be produced by China this year."

Gold hasn't lost its luster even as the Fed continues to raise rates – State Street's George Milling-Stanley

In the green energy transition, BMO said that silver demand within the solar sector will remain an essential factor in the precious metal.

"Even taking into consideration reduced silver intensity per cell, we still forecast PV silver demand to increase 8% to 123Moz by 2030, from 2021 levels, owing to the accelerated buildout of solar generation capacity. In a scenario where there is no further reduction in silver intensity, we would expect PV silver demand to increase to 160Moz by 2030," the analysts said.

The growing electric vehicle market also represents a growing source of demand for silver. BMO sees silver usage in the auto sector growing to 89 million ounces by 2030, up nearly 65% from 2021 levels.

"While we expect the gold:silver ratio in the long term to revert to 70:1, mounting recessionary signals, geopolitical tensions and still searing inflation could see the risk-off environment persisting in the near term, which on balance should favor gold above silver. Ultimately, tightening monetary policy will likely weigh on gold over the medium term, with silver more insulated from price corrections owing to the importance of industrial demand," the analysts said.

Cryptocurrency Has Changed the Dynamics of Savings and Investment: Will Banks Survive the Storm?

Cryptocurrency has changed the dynamics of savings and investment, but the effects of this change are not yet fully understood. This article discusses the impact of cryptocurrency on the global economy and the implications for banks.

Blockchain technology is revolutionizing the banking industry. As banks continue to evolve and adopt new strategies, they may need a strong understanding and implementation of blockchain technology if they want to remain relevant in the future.

A blockchain is a public ledger that stores data without a centralized intermediary such as a bank or government agency that could become corrupted by fraudulent transactions, data loss, or malicious behavior on its part. Instead, it relies on consensus protocols that ensure trust between all users on the network when recording financial transactions on the shared ledger across multiple participants (called nodes).

Blockchain technology provides a secure way to store information and track transactions because it is not stored in any one place but dispersed across multiple networks.

Background of the Digital Currency

Cryptocurrencies are a new form of digital currency that can be used to make purchases and transfer money anonymously. These currencies have no physical form and exist only in the digital world. The emergence of cryptocurrency has affected the banking industry: will banks survive the storm?

Cryptocurrency is decentralized, meaning any government or central authority does not control it. The transactions are verified through a process called mining, which involves solving complicated math problems with powerful computers to crack cryptographic codes. Blockchain technology enables cryptocurrency users to purchase goods and services online without having to worry about fraud or identity theft because all transactions are recorded on this shared public ledger for anyone to see.

The blockchain technology industry has been developing rapidly in recent years. Some projects are being used by well-known global organizations, including JPMorgan Chase and Accenture, to streamline the supply chain process. Others have been developed specifically for cryptocurrencies such as Bitcoin and Litecoin (although they can be applied to any form of digital currency).

However, despite the widespread interest in blockchain and how it could revolutionize business processes, there remains a lack of understanding among many businesses around its actual value and potential use cases, which limits their ability to benefit from using it.

Cryptocurrency has a significant impact on the global economy. It affects the exchange of goods and services and the transfer of funds from one country to another, weakening the foreign exchange rates. As of March 2022, there are approximately 18,000 cryptocurrencies in existence. The number of cryptocurrencies is growing daily and its market capitalization is estimated to grow to $5 trillion by 2025.

Blockchain technology has already penetrated many industries, including the financial sector, government, healthcare, media, retail, etc. However, many issues with cryptocurrencies still need to be resolved before they can be used in a mainstream society like traditional currency.

Its significant benefits of being fast, easy, cheap, and secure have been widely accepted and embraced by people worldwide for years despite some shortcomings such as volatility, lack of regulation, etc. The digital currency has been used in various ways so far, most notably for online gambling, but also as an alternative to fiat currencies in some countries where they offer a better exchange rate (and are sometimes even preferred).

The use case of cryptocurrencies is also evolving; while many people will continue to use them as a form of money or payment systems, many others might use them for trading, which includes buying goods and services; using cryptocurrency instead of fiat currency.

Cryptocurrency and the Banking Industry

Bitcoin, the first and most popular cryptocurrency, was created in 2009. It was created as a decentralized form of currency that is not controlled by any one country. It functions as a peer-to-peer payment system that does not require any middlemen, and a network of nodes verifies transactions.

Bitcoin and other cryptocurrencies have gained traction in recent years, but the regulatory environment for cryptocurrencies is still unclear. There are advantages to using cryptocurrencies, such as security, transparency, and no central control.

However, there are also disadvantages to using cryptocurrencies, such as price volatility, potential hacking, and lack of regulatory oversight. There are two sides to the cryptocurrency debate. One side argues that cryptocurrencies are the future of money and will replace cash, credit cards, and other payment methods. The other side argues that cryptocurrencies are a speculative bubble that will soon burst.

Some say that the implications of cryptocurrency on the global economy are not yet fully understood, but there are some apparent effects. For example, cryptocurrency has allowed individuals to transfer money internationally without banks or a third-party service. Cryptocurrency has also led to a decrease in demand for gold and other precious metals, as well as a reduction in cash usage.

The effects of cryptocurrency on banks are unclear. Some argue that banks will be irrelevant shortly, while others argue that banks will survive the storm. Cryptocurrency has caused a decrease in demand for banks' services and has led to an increase in financial risk. Banks may likely weather the storm by embracing cryptocurrencies and exploring new technologies like Blockchain. But will this ever happen? Who knows!

Roles of the Banking Sector in an Economy

In an economy, the banking sector plays a crucial role in facilitating the flow of money and providing loans to businesses and individuals. They have the power to regulate the money supply, which means they can determine how much money is in circulation.

This gives them control over inflation and deflation in the economy, so their actions must be responsible and transparent to avoid economic instability and financial crises such as the Great Recession from December 2007 to June 2009 and the recent financial crisis.

The central banks also determine whether the banks charge interest on loans and, if so, what the interest rate will be (known as the "prime rate" in the United States). Since banks can lend funds out of their reserves, there is a limit to the amount of capital they must hold; therefore, banks should borrow from other banks when necessary rather than from the public.

According to the conventional wisdom of financial economics, financial crises are inevitable in any economy that runs on fiat money because they occur when banks borrow more than they have and then fail to repay what they owe (Minsky, 1973).

The Federal Reserve System has attempted to prevent financial panics by keeping the supply of money constant and increasing it through open-market operations whenever the volume of outstanding debt increases by an amount greater than or equal to the Fed’s target for M1, which represents currency plus demand deposits at commercial banks. This method is commonly referred to as “monetizing the deficit.”

Why Are the Banks Cautious of Cryptocurrencies?

Undoubtedly, cryptocurrency has given rise to new, disruptive technology for money transfers and payment systems at large. Still, the central banking industry remains skeptical about its potential for displacing fiat currency as a medium of exchange or store of value, particularly when considering the risks associated with digital currencies like Bitcoin.

The cryptocurrency pioneer relies on decentralized networks and cryptography for security purposes instead of traditional regulation and oversight methods employed by central bank regulators worldwide and their regulatory bodies (the Financial Services Authority in the UK is an example).

Bitcoin has been around for over a decade and is the most well-known cryptocurrency. But as more and more digital currencies come into the marketplace, banks are starting to get cautious. They are concerned about potential losses resulting from transactions on these platforms. They don’t know what regulations governments will put in place to ensure these cryptocurrencies are not used for illicit purposes such as money laundering or terrorism financing.

One of the world’s largest bitcoin exchanges, Bitfinex, was hacked in August 2016 and had millions of dollars worth of bitcoins stolen from its customer's wallets and accounts. This has raised many valid questions about why the banks are concerned about the emergence of cryptocurrency.

Cryptocurrencies can also circumvent government-imposed capital controls, and it is now increasingly being used by international companies to avoid or evade taxes in various countries around the world.

This is due to the use of cryptography, allowing people worldwide to send funds to each other with complete anonymity and in a decentralized manner, using a peer-to-peer network of computers rather than a central server as traditional financial institutions do today.

However, because of its decentralized nature, bitcoin poses a risk of anonymous money laundering and terrorism financing, especially when combined with other forms of digital anonymity, such as “mixers” and other privacy-enhancing technology like Tor (The Onion Router) and VPNs (virtual private networks), which are used to mask IP addresses.

The latest trend in the financial sector is the rise of cryptocurrency. In 2009, a person or group under the pseudonym Satoshi Nakamoto published a paper describing digital currency. The paper introduced bitcoin, which became the first decentralized cryptocurrency in the world. Bitcoin and other cryptocurrencies have since become increasingly popular but also volatile.

For example, the price of Bitcoin rose from $2,500 in January 2017 to $19,000 in December 2017. Cryptocurrency is decentralized and relies on blockchain technology, and a central bank or government does not regulate Bitcoin and other cryptocurrencies. This makes cryptocurrency appealing to those weary of the unpredictable monetary policies of central banks and governments.

Many advantages come with cryptocurrency, such as its decentralized nature and independence from government interference, making it a great alternative to fiat currency systems (e.g the $USD).

However, it is essential to note that not all currencies have the same benefits as Bitcoin or other cryptocurrencies. It is also safe to say there is no guarantee that Bitcoin will be successful in the long run when compared to fiat currency, which has been around for thousands of years and has proven itself over time to be a stable medium of exchange for both individuals and businesses alike.

Nevertheless, if you look at the current state of cryptocurrency and the new development of blockchain technology today, many believe that it could be the future of money in this century. So they are trying to create more decentralized systems like Bitcoin or Ethereum, etc., but these systems are still in the early stages of development. We need more time before we can see what will happen with these currencies and applications.

So, for now, we need to find ways to secure our money from banks and other traditional financial institutions because as long as we have centralized systems that control how much currency and transactions are allowed, it is very easy for them to steal your funds or freeze your account whenever they deem it necessary.

In Summary

The Central Banks are at the heart of the modern global financial infrastructure in the current economic system, and as such, they have become a powerful force in society. In many cases dominating the economic life of nations to the extent that can be likened to that of feudal rulers controlling their kingdoms and duchies during times past.

Today we have what amounts to the equivalent of the Royal Family controlling central banks worldwide! In recent years, with the onset of a global economic collapse and with the Federal Reserve’s power over the American economy and the global economy increases, the Federal Reserve has become ever more influential over the entire planet.

Blockchain technology depends on algorithmic confidence, and its decentralized system offers an option to the current system. But the cryptocurrency has little adoption rates, and its legal reputation is still under the cloud. Cryptocurrencies are a new digital asset class with no central authority or bank behind them.

Instead, it relies on a distributed network of computers and users to maintain order and security in exchange for incentives and rewards, which is why they are often called “digital cash” as opposed to more traditional means of storing value like paper currency and gold. Many different cryptocurrencies are available today: Bitcoin Cash, Litecoin, Ethereum, Ripple, Dash, Zcash, Monero, Dogecoin, and so on.

There are possibilities at this point that Central Banks will start to introduce their own central bank digital currencies (CBDC). The problem is that nobody has yet been able to provide a solution for what happens when CBDCs across international borders fail. The associated costs and risks become more challenging to manage than they currently are today for national fiat currency systems.

The global financial system remains reliant on national monetary policymakers being willing to let the exchange rate of their respective countries weaken over time as part of ‘internal devaluation to encourage domestic consumption and investment spending via the money multiplier mechanism – something that can only be achieved if there are sufficient savings available.

Federal Reserve raises rates ¾%, addressing inflation at 8.6% the highest YoY spike since December 1981

The Federal Reserve took the most aggressive action since 1994 announcing that they would raise rates by 75 basis points (3/4%) taking the fed funds rate to between 150 – 175 basis points. Traders and analysts had been factoring in a more aggressive rate hike on Monday and Tuesday following the release last week of the May inflation numbers vis-à-vis the CPI. Inflation rose to the highest level since the start of the pandemic which led to a recession that was followed by other disruptive events including extreme supply chain bottlenecks, Russia’s invasion of Ukraine, and Covid-related lockdowns in China.

The Federal Reserve’s statement concluded, “Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.”

The Federal Reserve statement said that the issues mentioned are the primary reasons that members of the Federal Reserve decided to raise their target interest rates to 1 ½% – 1 ¾%. The Fed also anticipates that interest rates will continue to increase to above 3% by the end of 2022.

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 1â1/2 to 1-3/4 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt, and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve's Balance Sheet that were issued in May. The Committee is strongly committed to returning inflation to its 2 percent objective.”

The Federal Reserve has long maintained a dual mandate of maximum employment and an inflation rate of 2%. Chairman Powell alluded to a strong possibility that there would be more 75 basis point rate hikes at the next FOMC meeting in July. During his press conference Chairman Powell said that further rate hikes of either 50 or 100 basis points would “most likely” be the appropriate outcome of the central bank’s next meeting in July.

Today’s statement also addressed the Fed’s current economic outlook which anticipates an economic contraction taking the GDP growth rate to 1.7% this year, unemployment rising to 3.7%. Furthermore, they are forecasting that unemployment will rise to 4.1% through 2024. These numbers indicate that it is obvious to the Federal Reserve that its plan to continue to raise interest rates will lead to a further economic contraction and a higher unemployment rate. The committee also acknowledged that inflation levels will remain elevated with the PCE index trending at approximately 5.2% throughout the remainder of this year and gradually reducing to 2.2% in 2024.

The Federal Reserve’s aggressive rate hike and downward revision of GDP were factored into market pricing over the last two trading days. That being said. I still believe that market participants' reaction to today’s aggressive rate hike and downward revision of their economic outlook was an odd one resulting in U.S. Treasury yields moving lower, dollar weakness, along with rallies in U.S. equities and the precious metals markets.

Gold futures gained $22.80 and as of 5:20 PM EDT, the August contract is currently fixed at $1836.10. Silver futures gained 3.51%. The September contract gained almost $0.74 today and is currently fixed at $21.69. This is the opposite reaction for gold and silver prices than was anticipated after the Fed announced the aggressive 75-basis point rate hike today.

The Great Migration of Americans Out of Dysfunctional Cities

by Doug Casey, founder, International Man Communique

International Man: After the outbreak of the Coria and subsequent government actions, many Americans decided to move to a new state.

For example, it's estimated that 319,020 residents fled New York state between July 2020 and July 2021, which amounted to about 1.6% of its population. It was the largest outflow of any state during this period.

What is going on here?

Doug Casey: It's quite simple and obvious: people are getting away from what they don't like.

In essence, that means taxes, regulations, corruption, street crime, and a "woke" social ambiance. These are all things that relate to government. As late as the 1950s, the local government wasn't a major factor when deciding where to live. Now it is.

Some states now have up to a 13% income tax, and some have 8 to 10% sales tax. These are huge considerations where they were once trivial. So there's a huge difference between various states regarding the costs imposed upon you by the government.

Generally speaking, the highest tax states are also the most woke and the most regulated. That's because the wokesters approve of high taxes in principle. They believe a big government is good and necessary. Furthermore, the high taxes go to promote woke policies. So high taxes and woke policies naturally reinforce each other.

The places with the most woke governments and highest taxes generally have the highest levels of welfare spending, which draws in a certain type of person. As a result, they have hundreds, or even thousands, living on the streets.

They used to be termed "bums" or "vagrants." Then you were supposed to call them "the homeless." That sounded better because it didn't imply a moral failing, just the lack of a permanent residence. Now, however, you're supposed to call them "the unhoused." This further softening seems to imply that they just don't have a house for the moment—that sounds no worse than not having a car, airplane, or perhaps a diamond ring, or maybe a pension. They're "underprivileged" and should have a home in our hearts. No moral failing there.

I prefer to call these people bums, the traditional term. But it's almost passed out of the language. It should be re-instituted. It's crazy what the progressives and the wokesters have done to the language. Their euphemisms have made words as dishonest as their policies and philosophies.

Places like New York, Baltimore, Chicago, San Fran, and scores of other liberal bastions have the worst crime because they draw in and retain the worst kind of people—those who want to take advantage of their woke policies. And they scare away people who value the opposite values—hard work, prudence, temperance, self-reliance, justice, and the other traditional virtues. The politicians in these places promise bread and circuses to the degraded hoi polloi in exchange for their votes. They draw in the worst people and scare away the best. It's a self-reinforcing type of situation that can become a death spiral. The US is no longer a democracy but a kakistocracy.

Although moving can be inconvenient, it's insane to stay rooted in a place that's degrading, with the worst conditions but the highest costs. Get a load of this article written by a liberal in "The Atlantic."

International Man: How have the policies the local politicians enacted led to these conditions?

Doug Casey: People who get into politics are generally narcissists. They're interested in popularity. Their priority isn't the good of society but self-aggrandizement. They don't create anything and can only take from some people and give to others.They do what's good for themselves, building their own brand names, hoping that successful manipulation of the hoi polloi will enable them to move from being a big shot in their municipality to a big shot in their county, then a big shot in their state, and finally making the big time in Washington DC.

What's going on here? Why do people support their destroyers? How is it that, of all animals, only humans install the most venal and stupid as their leaders? There must be some basic flaw in humans that, at least when they're in a large enough group, causes them to act irrationally. Why else would people support the kind of people who want to be politicians?

It doesn't matter whether they're Democrats or Republicans. Although I've got to say that in many ways, I respect the Democrats more than the Republicans. That's because the Democrats, as bent as they are, at least have a philosophical center. They actually believe in some things—even if they're bad things. The Republicans, however, don't believe in anything—except that the Democrats are just moving too far and too fast towards statism and collectivism. That makes the so-called conservatives hypocrites, allowing the so-called liberals to masquerade as the party of principle.

Neither the Democrats nor the Republicans are worth the powder it would take to blow them to hell. As H.L. Mencken correctly said, politicians are America's only native criminal class.

It's foolish and a moral, philosophical, and—usually—a practical mistake to support either of them. Both should be decried. Don't feed either Tweedledee or Tweedledum. They're the problem, not the solution.

International Man: While New York saw the largest outflow of residents, Texas and Florida were among the top recipients of new residents.

What do you think the long-term impacts will be on these states, and what are the implications?

Doug Casey: There are two possibilities.

Many of the emigrants are so shallow and thoughtless that they don't realize that it was their own views and habits that destroyed the places they want to get out of. They're likely to take many of their stupid ideas and bad habits with them because they can't change their basic psyche. They can't reform their basic worldview. Most don't think logically about cause and effect.

But some may have been mugged enough by the reality that they've changed their views. Some are ethically upright but have just been buried in a negative environment. I have a number of AnCap friends who started out as Marxists. So there's always hope…

But my guess is that most of the people moving from New York and California to places like Texas and Florida are reasonably conservative, rational people. That's why they're moving. So most of them will actually reinforce and improve the situation in their new states. So it's cause for optimism. Perhaps it will lead to the secession of some regions.

A bigger problem is that the country, as a whole, still seems to be moving more statist. The Blue people—the socialist-leaning people—have control of the State apparatus most everywhere. And once they have control of the apparatus of the State, it's very hard to take it away from them.

Worse yet, as the economy goes into a real crisis with the Greater Depression deepening over the next few years, both the Red people and the Blue people will clamor for a man on a white horse who will claim to kiss everything and make it better—if he has enough power.

International Man: Many formerly prosperous US cities have degenerated into conditions more akin to an impoverished Third World country in certain areas. This trend shows no sign of reversing and seems to be accelerating.

What is the cause of this, and where is this all headed?

Doug Casey: As I've said many times in the past, science fiction is a better predictor than any think tank of what's likely to happen.

Let me draw your attention to the Kurt Russell movies Escape from New York and Escape from LA, showing how dystopian big cities can get. And the earlier Charles Heston/ Edward G. Robinson movie, Soylent Green. Could things get that bad? Yes, they could. The more advanced civilization gets, paradoxically, the more unstable it can become if the foundations aren't sound. We discussed why the foundation is crumbling in our last two conversations (link here and here)

Look at ancient Rome. It had a million or more people at the time of Caesar Augustus. But after the collapse of the empire, the population fell to perhaps 20,000 people during the dark ages that followed. Cows and goats grazed in the forum. The peasants disassembled Rome's buildings to have something better than straw shacks to live in.

Civilizations and cities have collapsed many times in the past 5000 years. It could happen to New York, Chicago, San Francisco, or the US itself—unless they radically change their policies. But, notwithstanding the recent recall of SF's disastrous district attorney, there's no indication that they will. In fact, most jurisdictions are raising taxes so the government can "do more." Which, of course, just makes things worse for the reasons we just discussed.

Take a look at Detroit. There are 20 and 30-story office buildings downtown with market values of only a few million dollars. During the 1950s, Detroit was the fourth-largest city in the country and one of the wealthiest.

How do we turn the situation around? It's not by voting. That just transfers power from Tweedle Dee to Tweedle Dum. But that doesn't mean you should be quiet and say or do nothing. For that reason, I try to speak out whenever I hear people saying things that are commonly accepted but destructive.

In that regard, let me mention a club that I belong to here in Argentina. It's a group of American businessmen who get together for lunch every two weeks and talk about the world at large.

At our last meeting, an American/Argentine dual citizen went on about how politicians ought to say this or not say that—whatever works—to get people to vote for them. Our James Carville lookalike tells politicians how to appeal to the masses. He particularly spoke out against Javier Milei, an AnCap who—rather improbably—has a serious chance of becoming the next president because he threatens to overthrow the country's totally corrupt Peronist/Kirchnerite system.

I couldn't let that pass and commented that not only is politics itself the problem, but the worst people go into politics. And those who instruct politicos on how to manipulate the hoi polloi are the worst of all. I took the opportunity to broach the thought that the State was their enemy, and its powers to tax, regulate, and inflate the currency should be ripped out by the roots, with Agent Orange poured on the ground they grew in.

Will my words change anything? No. But I told them that these things need to be said. Otherwise, the enemy's victory is certain. We're fighting a psychological and philosophical war.

International Man: What is your advice to people considering moving to a new city, state, or country.

Doug Casey: Things will continue to deteriorate for the foreseeable future. Trends in motion tend to stay in motion, and this trend is still accelerating. Actual Jacobins and Bolsheviks will be running the US for at least another 30 months.

However, if you want to stay in the US and you live in a major city—it doesn't matter where—I would move to a rural area. People in rural areas are closer to the earth and reality. They have more traditional values and fewer bad habits. Their general worldview is more conservative. In big cities, it's always more liberal. Like tends to draw like. In cities, urban gangs may start taking over in "no go" zones.

Let me draw your attention to another seminal sci-fi movie from the early 1980s, The Warriors. You'll recall that New York seemed on the edge of collapse back then. One of the movie's subplots posited the gangs of New York uniting to take over the city and how they almost do it. It could happen.

There's every reason to move to a rural community. Costs are always much lower, while modern telecommunications, FedEx, Amazon, Walmart, and the rest of it give you all the material advantages of living in a big city with much less crime and fewer wokesters.

The only reason not to move to a small town is if you're still in your twenties or maybe thirties, unmarried, and want to be in the dating scene. Small rural towns aren't very active from that point of view. But otherwise, there's every reason to live in the countryside as opposed to the big city today.

If you're going to stay in the US, move out of the city, pick a nice small town, and beat the last-minute rush.

New Opportunities Are Emerging For Citizens of The World.

Freedom and democracy may appear to be struggling to stay alive in America, but there may be a knock-out punch ready to be released. The evolution of the blockchain-enabled metaverse is going to enable the 'Citizens of the World' to gain their own Freedom by democratizing power and creating a new world with new rules, new players, and new opportunities. For 99.99% of us, the metaverse will improve our real-world lives through the democratization of power and opportunity.

Along with the major long-term trend of society towards decentralization and smaller-scale organizations, there are new opportunities developing to help 'Preparers' in the cryptocurrency sector. Businesses are beginning to issue their own Crypto Coins that can be traded on Cryptocoin Exchanges.

Markethive.com for example will be releasing its HiveCoin (HIV) in the coming weeks. It has tremendous upside potential that is outlined in a Video by Founder Tom Prendergast, "Entrepreneur Advantage…".

Not only that, if you go to their website and register as a FREE Member, you will be given 500 HiveCoins for "FREE" along with access to several Earning Opportunities and online tools to increase your HiveCoin balance.

The Food and Agriculture Organization (FAO) of the United Nations, headquarters located in Rome, was established in October 1945 by the United Nations assembly in the wake of World War 2. Its aim is to improve nutrition and living standards, agricultural productivity, and the conditions of farmers and make the best use of the world's food resources. It provides food and nutrition advice, technical assistance, and other support to people in need in both emergency and non-emergency situations.

During a meeting on 8th June 2022, FAO Director-General, Qu Dongyu, participated with dozens of ministers at the summit in Rome to tackle higher prices for food, fertilizer, and fuel. Acknowledging a “very complicated” global scenario, he urged countries in the Mediterranean to work together to mitigate food security risks that the war in Ukraine has further exacerbated.

The Mediterranean Sea region includes 22 countries on three continents, each with diverse natural resources, agricultural traditions, and production potential. The Ministerial Mediterranean Dialogue on Food Crisis, an event convened by Italy’s Minister of Foreign Affairs, Luigi Di Maio, drew ministers and government participants from more than 24 countries.

Minister Luigi di Maio opened the Dialogue, noting that seldom has hunger had such a high profile on the public agenda and emphasizing the importance of sustainable agrifood systems.

Qu noted that,

“We must keep our global food trade system open and ensure that agrifood exports are not restricted or taxed.”

More investment in countries that are severely affected by the current increase in food prices.

Reduction of food loss and waste.

Better and more efficient use of natural resources, especially water and fertilizer.

A focus on technological and social innovations that can significantly reduce market failures in agriculture.

“We are facing the worst food crisis in decades,” said Svenja Schulze, Germany’s Minister for Economic Cooperation and Development, who co-chaired the event.

Participants agreed that high prices for fertilizers and fuels, both critical agricultural inputs, are urgent matters for global food security.

European countries are now looking at options for compensation for individual industries, which have enormously high costs due to energy prices.

Before the war in Ukraine began, the European Union was an exporter of grain, like Ukraine and Russia. Export from Ukraine went mainly to the Middle East and North Africa. But that is likely to change now.

The Arab states now have grain stocks purchased, so prices would not have to go up again in the autumn. So far, the harvest looks good in the rest of Europe, but also in countries such as Australia and Canada.

Rising food prices could stabilize after this year's grain harvest, estimates the Food Chamber of the Czech Republic. According to her, current agricultural prices are speculative, with a good harvest, growth could calm down.

Following this, the prices of feed, flour and meat would no longer have to rise – however, food will not return to last year's values."An absolutely crucial signal will be how this year's harvest ends, because prices now do not fully reflect reality," said Miroslav Koberna, director of the Chamber of Programming and Strategy of Czech Republic.

How Do Food Process Compare Across Europe?

Food prices are skyrocketing across Europe. In some countries, however, it does not burden people's wallets as much as in the Czech Republic. Experts say that this is due to higher incomes and different levels of food taxation.

In the Czech Republic, most foodstuffs are subject to 15% VAT. But some states are more lenient. For example, in Poland, several foods are not subject to VAT. They have a similar situation in Hungary.

For example, according to the so-calledBig Mac index, the famous hamburger Big Mac earns the fastest in Luxembourg or Switzerland; it takes them about ten minutes. The longest then on one Big Mac they work in Ukraine, almost an hour. It'll take the Czechs about half an hour.

Czech households spend 17.1% of their income on food, which is close to the European average. A quarter of the senior pension falls on basic foodstuffs in the Czech Republic. Comparing Czech food prices – in Italy are 22% more expensive. Lower prices of foods are in Bulgaria and Poland, about 20-25% more than in Czechia are the food prices in Greece, Austria, Italy or France.

In Czechia, the prices of foods in comparison to last year grow extremely. In May 2022 flour prices accelerated to 64.6% year on year, for butter to about 52 %, for semi-skimmed long-life milk to about 42% and for eggs to about 34%.

“Yellow prices” are reduced – very often quickly sold out

People in Ireland or Scandinavia spend the least on food. On the contrary, they pay the most for them in Romania and the Baltic states. In Germany the average income is about three times more than the Czechia, so of course Germans can afford to buy more food, says one Czech economist.

European countries are currently dealing with compensation options for individual sectors, which have enormously high costs due to energy prices.

Germany will pay about 32 million euro, Poland 800 000 euro and France will according to experts be the clear winner in the food industry due to its highest investments in rescuing processors.

Food Inflation In Europe – The Numbers Say it All

This table shows the percentages of inflation in European countries – highest inflation in food prices has Moldova with 30.2%, second place is Lithuania with 24.8% and so on. Absolutely in the best situation is Switzerland with only 1.1% food inflation.

Gold, silver continue sell off amid strong greenback, rising bond yields

Gold and silver prices are solidly lower in midday U.S. trading Tuesday, with both metals notching four-week lows. A strong U.S. dollar index that this week hit a 20-year high and U.S. Treasury yields that this week hit multi-year highs are significantly bearish elements keeping the metals prices under selling pressure. Gold and silver bulls got no help from another hot U.S. inflation reading today. August gold futures were last down $19.60 at $1,812.10. July Comex silver futures were last down $0.400 at $20.855 an ounce.

Today’s U.S. producer price index report for May came in a up 10.8%, year-on-year and up 0.5% from April. Those numbers were close to market expectations and the markets showed no major reaction. But make no mistake: inflation in the U.S. and around the globe is running hot and is problematic. History shows problematic price inflation is longer-term bullish for hard assets, including the metals markets.

Global stock markets were mostly lower overnight. U.S. stock indexes mixed at midday. The U.S. stock indexes are in bear market territory, meaning they are down 20% or more from their highs. Despite today’s stabilization in the U.S. indexes, traders and investors see their risk appetites as far from robust.

The data point of the week is the Federal Reserve’s FOMC meeting that began Tuesday morning and ends Wednesday afternoon with a statement. The Fed is expected to raise U.S. interest rates by at least 0.5%. Some reckon the Fed may raise the key Fed funds rate by 0.75%. Fed Chairman Jerome Powell will hold a press conference after the FOMC meeting concludes Wednesday afternoon.

Markets in chaos: Gold price down $50, Bitcoin price hits lowest level since December 2020, stocks plunge

The key outside markets today see Nymex crude oil prices higher and trading around $122.25 a barrel. The U.S. dollar index is firmer in midday trading and not far below this week’s 20-year high. The yield on the 10-year U.S. Treasury note is fetching around 3.3%. Monday the 10-year note hit the highest level in 14 years, at 3.371%.

Crypto currencies remain under strong selling pressure again, with Bitcoin at a 1.5-year low.

Technically, the August gold futures bears have the firm overall near-term technical advantage. Bulls’ next upside price objective is to produce a close in June futures above solid resistance at this week’s high of $1,882.50. Bears' next near-term downside price objective is pushing futures prices below solid technical support at $1,800.00. First resistance is seen at the overnight high of $1,833.30 and then at $1,850.00. First support is seen at the overnight low of $1,809.20 and then at $1,800.00. Wyckoff's Market Rating: 2.5

July silver futures bears have the solid overall near-term technical advantage. Silver bulls' next upside price objective is closing prices above solid technical resistance at the June high of $22.565 an ounce. The next downside price objective for the bears is closing prices below solid support at the May low of $20.42. First resistance is seen at today’s high of $21.36 and then at $21.75. Next support is seen at $20.42 and then at $20.00. Wyckoff's Market Rating: 2.0.

What's next for crypto after 'perfect storm' crashes prices? Ethereum's market cap is 'orders of magnitude higher' than Bitcoin — Messari

What's next for crypto after 'perfect storm' crashes prices? Ethereum's market cap is 'orders of magnitude higher' than Bitcoin — Messari

.jpg)

Gold hasn't lost its luster even as the Fed continues to raise rates – State Street's George Milling-Stanley

Gold hasn't lost its luster even as the Fed continues to raise rates – State Street's George Milling-Stanley

.png) Image courtesy of

Image courtesy of  âââââ Image Courtesy of

âââââ Image Courtesy of