Will the Fed stop gold's run? Gold price sees longest weekly winning streak since the summer of 2020

Gold is looking to close Friday with its sixth weekly gain — the longest winning streak since the summer of 2020 when gold hit new record highs above $2,000 an ounce. But the question is whether the precious metal can maintain its rally as analysts see inevitable profit-taking in the short term.

One argument analysts raise for next week is why wouldn't gold investors take some profits off the table after seeing stellar gains this January.

Earlier this week, gold was up more than 6% year-to-date — the best start to the year since 2012 — as the precious metal hit a fresh nine-month high at around $1,949. At the time of writing, February Comex gold futures were last at $1,930 an ounce, up 0.10% on the week.

"With big data points coming in, the market will back off, and you will take profits off that table," Walsh Trading co-director Sean Lusk told Kitco News Friday.

The top event to watch next week is the Federal Reserve meeting on February 1, followed by central bank Chair Jerome Powell's press conference.

There is a lot of noise regarding the pace of rate hikes potentially slowing down, Lusk said. But the Fed could still surprise with a hawkish stance.

Markets are currently pricing in a 98.9% chance of a 25-basis-point hike next week, according to the CME FedWatch Tool. But Lusk is not ruling out a 50-basis-point move. "I don't think the Fed will be less aggressive as they are looking at the long term," he said. "With China opening up, there will be more demand. The Fed could keep its foot on the pedal here."

Lusk warned that a move below $1,917 an ounce could trigger a drop to $1,920, and then the market is at risk of re-testing $1,890 and $1,860 levels. "I wouldn't be surprised if we saw a wipeout. We had a big rally since early November," he said.

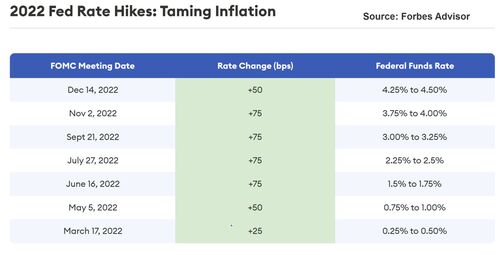

The market believes the Fed is close to being done, OANDA senior market analyst Edward Moya told Kitco News. However, with too much inflation in the system, the Fed could signal that more needs to be done. "The Fed is sticking to the dot plot — 25 bps, 25 bps, and 25 bps," Moya said.

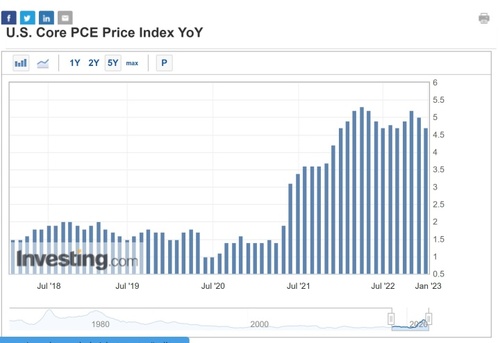

The Fed's preferred measure of inflation — the core PCE index — told an interesting story Friday, Moya added. "It showed that annual inflation is still more than twice the Fed's target. And the month-on-month basis, it rose and snapped a streak of declines," he noted. "Gold will be a tough trade going into the Fed. And what it does after will be key."

Many analysts see gold as overbought at current levels. TD Securities noted that gold had been driven by massive Chinese purchases leading up to the Lunar New Year.

"Even more important than the Fed meeting will be the first signs whether massive Chinese buying is continuing post-Lunar holidays. This is one of the larger drivers for gold," TD Securities senior commodity strategist Daniel Ghali told Kitco News.

Longer-term, the majority of analysts are bullish on gold. "The upward trend is still intact," RJO Futures senior market strategist Frank Cholly told Kitco News. "I am disappointed the market hasn't managed to get above $1,966. We had quite a run, and the market is getting a breather," Cholly said.

Once gold can get above $1,966 an ounce, prices will shortly see the $2,000 an ounce level, Cholly added.

Data to watch next week

Another key event to keep a close eye on next week is the U.S. jobs report from January. Markets expect to see additional 185,000 positions added, with the unemployment rate climbing to 3.6% from 3.5%.

"Employment creation remains strong for now, but job lay-off announcements are coming in thick and fast," ING's chief international economist James Knightley said. "We expect to see a softer nonfarm payrolls increase than seen in recent months, but it is still likely to be well above 100k given the large number of job vacancies that remain."

Also on the radar next week are the European Central Bank and Bank of England monetary policy meetings.

Tuesday: U.S. CB consumer confidence

Wednesday: Fed meeting, U.S. ADP nonfarm employment, U.S. ISM manufacturing PMI

Thursday: ECB meeting, BoE meeting, U.S. jobless claims, U.S. factory orders

Friday: U.S. nonfarm payrolls, U.S. ISM services

By Anna Golubova

For Kitco News

Tim Moseley

.gif) The world could run out of gold by 2050 as demand grows to keep up with evolving society, says researcher

The world could run out of gold by 2050 as demand grows to keep up with evolving society, says researcher.gif)

.gif) Royal Mint sees record bullion demand in 2022 as sales increase 25% for gold, 29% for silver

Royal Mint sees record bullion demand in 2022 as sales increase 25% for gold, 29% for silver

With gold ending the week above $1,900, analysts turn their focus to $2,000

With gold ending the week above $1,900, analysts turn their focus to $2,000