Central banks' gold holdings drop for the first time in over a year in April, says World Gold Council

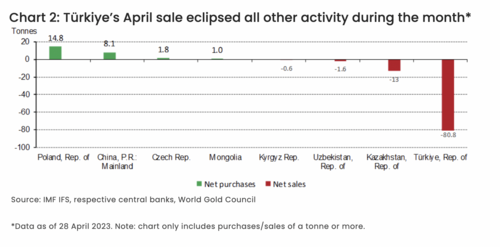

Global central bank gold holdings fell for the first time in more than a year in April, as Turkey sold over 80 tonnes of gold, the World Gold Council (WGC) said in a report.

Total central bank gold reserves dropped by 71 tonnes in April. The last time central bank gold holdings declined was in March 2022, and the net drop was one tonne, the report pointed out.

The monthly decrease is not representative of a trend reversal, said WGC's senior analyst Krishan Gopaul. "Country-level data reveals that, far from a sudden wave of central bank selling, the drop in reserves was primarily due to Türkiye," Gopaul said Friday.

The Central Bank of Turkey sold 81 tonnes of gold in April, reducing its gold holdings to 491 tonnes. This was after the central bank already sold 15 tonnes in March.

Last year, Turkey bought the most gold out of all central banks, purchasing 148 tonnes and increasing its gold reserves to 542 tonnes — the highest level on record.

The report explained that country-specific circumstances led Turkey to offload some of its gold.

"This was a specific response to local dynamics rather than a change to their long-term gold policy: the gold was sold into Türkiye's domestic market to satisfy very strong bar, coin and jewelry demand following a temporary partial ban on gold bullion imports," the report noted. "It remains to be seen if this selling will continue and, if so, at what pace."

Other sales in April were significantly smaller tonnage-wise. The National Bank of Kazakhstan sold 13 tonnes, the Central Bank of Uzbekistan offloaded two tonnes, and the National Bank of the Kyrgyz Republic sold 0.6 tonnes.

While massive gold selling is not likely to become the new trend, central bank gold purchases are slowing down.

Only four central banks bought gold in April, with Poland reporting additional 15 tonnes, the People's Bank of China buying eight tonnes (its sixth monthly purchase in a row), the Czech National Bank adding two tonnes, and the Central Bank of Mongolia purchasing an additional tonne.

The WGC is looking past April's drop in central bank gold holdings and projects more buying throughout 2023.

"Our view is also supported by findings from our latest Central Bank Gold Reserves survey, which shows reserves managers remain broadly positive towards gold," Gopaul said. "It's also worth noting that the Central Bank of Iraq recently announced a 2.5t purchase in May and signaled more to come."

Turkey's case is unique

Turkey has seen a surge in gold demand in the past year as citizens embraced the precious metal as a hedge against inflation, political and economic uncertainty, and local currency devaluation.

"Local demand for gold in Turkey is simply a desire to protect their purchasing power from a declining Lira," William Stack, financial advisor at Stack Financial Services LLC, told Kitco News. "Gold is a great asset to own when you are in a financial pinch because it can be sold when necessary."

Rising gold demand led to a jump in gold imports, which weighed on Turkey's widening current-account deficit. In response, Turkey introduced steps to curb gold imports in February and began selling its gold reserves to meet domestic demand.

But the move to offload some of its gold is not necessarily a losing scenario for the Turkish central bank, Stack pointed out.

"One reason Turkey is selling is that gold has risen 10% from a year ago, in dollar terms. In Lira-terms, the gain is more dramatic — 70-85%," he explained. "If Turkey sold gold internationally, it would weaken the Lira further. But when they sell gold to Turkish residents for Lira, it reduces the amount of Lira in the marketplace, thereby helping to strengthen the currency."

Gold, silver gain on ideas FOMC will pause at next meeting

Gold and silver prices are solidly higher in midday U.S. trading Thursday, amid a big U.S. economic data dump that culminates with Friday morning's U.S. jobs report. The precious metals are boosted today by ideas the Federal Reserve may pause in its interest-rate-hiking cycle. August gold was last up $15.80 at $1,997.90 and July silver was up $0.403 at $23.985.

The Wall Street Journal reported today the Fed is likely to pause in its rate-hiking cycle at the June FOMC meeting, before raising rates again later this summer. That's a shift from the consensus marketplace belief just recently that the Fed would again raise rates at the June FOMC meeting. However, a "sizzling jobs report" on Friday would throw cold water on the Fed pause, said the Journal report.

There was a very heavy U.S. economic data slate Thursday. The data was a mixed bag but the ADP national employment report for May did run hot, showing a rise of 278,000 jobs—well above market expectations. Traders are now looking ahead to the Labor Department's employment situation report for May on Friday morning. The key non-farm payrolls number is seen coming in at up 190,000 compared to the April non-farm jobs number of up 253,000.

Asian and European stock markets were mostly higher overnight. U.S. stock indexes are higher at midday. The marketplace has been assuaged by the U.S. House of Representatives handily passing the government debt-ceiling-extension deal reach between Republicans and Democrats. The measure now goes before the Senate and is expected to also pass.

Bitcoin voters could decide close U.S. elections as bipartisan political support grows – Lyn Alden

The key outside markets today see the U.S. dollar index solidly lower. Nymex crude oil prices are solidly higher and trading around $71.00 a barrel. These two outside markets were also bullish elements for the metals markets today. Meantime, the benchmark 10-year U.S. Treasury note yield is presently fetching 3.677%.

Technically, August gold futures bulls have the overall near-term technical advantage. Bulls' next upside price objective is to produce a close above solid resistance at $2,050.00. Bears' next near-term downside price objective is pushing futures prices below solid technical support at this week's low of $1,949.60. First resistance is seen at $2,008.00 and then at $2,020.00. First support is seen at $1,985.00 and then at today's low of $1,970.10. Wyckoff's Market Rating: 6.5

July silver futures bulls and bears are back on a level overall near-term technical playing field. A four-week-old downtrend on the daily bar chart has been negated. Silver bulls' next upside price objective is closing prices above solid technical resistance at $25.00. The next downside price objective for the bears is closing prices below solid support at $22.00. First resistance is seen at $24.40 and then at $24.75. Next support is seen at today's low of $23.355 and then at $23.00. Wyckoff's Market Rating: 5.0.

July N.Y. copper closed up 800 points at 371.70 cents today. Prices closed nearer the session high. Short covering was featured. The copper bears still have the overall near-term technical advantage. Prices are still in a six-week-old downtrend on the daily bar chart. Copper bulls' next upside price objective is pushing and closing prices above solid technical resistance at 390.00 cents. The next downside price objective for the bears is closing prices below solid technical support at 350.00 cents. First resistance is seen at today's high of 373.15 cents and then at 377.50 cents. First support is seen at this week's low of 362.20 cents and then at 360.00 cents. Wyckoff's Market Rating: 4.0.

In this article, I examine the concept and process of geoengineering as it relates to climate change, with particular scrutiny on whether geoengineering is solving a problem or engineering a problem.

As we continue through to the halfway point of 2023, the so-called emergency issues of the climate have once again come to the fore as the health topic of covid 19 regresses somewhat, although, as we shall see later, none of these things are standalone events.

As I write this article, pilot sites have sprung up in England, which are trial runs of 15-minute cities. It is based on the idea that everything you need can be accessed within a 15-minute radius. If you venture out of that zone, you risk fines and possible imprisonment. It is directly connected with the climate agenda, which you can read more about in Agendas 21 and 30.

I start with a speech by Prince Charles where he spoke of the need for a war-like approach to climate change in the form of a military-style campaign. On reflection, it sounded like more of a confirmation of something that was already happening.

What has humanity done to deserve such impending and extreme restrictions, with all the hallmarks of a more permanent lockdown? Let’s start with some definitions of the issue at hand.

The reported ‘climate crisis’ appears to stem from a belief about the threat of global warming to the survival of this planet. Regular conventions and summit meetings have been held since the 1960s to discuss the severity of this perceived issue and plan accordingly. In tandem, there have also been summit meetings on population control, such as the International Conference on Population and Development in Cairo in 1994, suggesting that both themes are connected.

Here is a video of scientist Carl Sagan explaining the greenhouse effect to Congress. According to the Council for Foreign Relations, there is a consensus of opinion about the science concerning climate change.

They cite a summary of that science from David Victor, an American Professor of International Relations, who summarises that the earth's temperature is rising at unprecedented rates, which will result in damaging effects across the world.

He puts this down to human activities using fossil fuels, deforestation, coal, oil, and natural gas. As a consequence of these activities, greenhouse gasses such as carbon dioxide have been emitted in sufficient amounts to cause the planet to trend toward global warming.

There are a group of climatologists that dispute this stance in that they claim there is no emergency as such. These include climatologists Dr. Judith Curry and Dr. John Christy.

Moreover, a global network of over 1100 scientists and professionals known as the “Global Climate Intelligence Group” or The CLINTEL Group has prepared an urgent message explained in this article.

Perhaps the use of the phrase climate change is something of a tautology since the earth is not a static ecosystem. If indeed there is a climate crisis, is it as described by the powers that be, or does the issue lie elsewhere?

FALSE PROPHECIES or INEXACT SCIENCE

Since as far back as the 1960s, many global leaders and political figures have been sending out alarming warnings in the form of predictions. This X22 report cites some of them from a Twitter feed. Here is a paraphrase of some of the identified warnings:

1966 – No more oil in 10 years

1967 – Dire famine forecast by 1975

1970 – Nitrogen build-up will make all land unusable

1970 – Ice Age by 2000

1974 – Ozone depletion will make life perilous

1980 – Acid rain will kill life in lakes

1989 – Rising sea levels will obliterate nations if nothing is done by 2000

2008 – Al Gore predicts an ice-free Arctic by 2013

2009 – British Prime Minister says we have 50 days to save the earth

None of the above has come to pass. This poses a fundamental question. Bearing in mind that science and political science are not one and the same, are the above merely false prophecies from the domain of political science, or is it a case of science not being so exact as to be predictable?

Maybe both have some truth to them, yet as this short clip about an ongoing project in Greenland shows, context and relativity are essential in research. In this project, ice is extracted from the ice sheet in Greenland over thousands of years to determine temperatures during that time.

Their results underline that when certain political authorities raise the alarm about the increase in warming by 1.5 degrees, they need to put relativity in context. In isolation, you can make research support many inaccurate viewpoints.

There is a third, more serious consideration when we consider context and the interface with political science. What if the political powers in question are creating the problem and then creating a solution to put the control of power firmly in their domain?

To appreciate why this is an important consideration, I refer to the book The Creature from Jekyll Island by G Edward Griffin, a highly acclaimed documentarist and writer with a flair for taking the complexity out of complex subjects to make them easier to understand. This book first came out in 1994.

Although the creature referred to in the title is the Federal Reserve, and the book focuses on the nature of its creation and the money agenda, various interconnected threads arise in his discovery which has a direct bearing on the climate agenda.

Griffin makes reference to the influence of the Fabian School of Economics in London, whose underpinning ideology was the achievement of a new world order by a more covert expression of socialism as opposed to a more forceful approach, such as what is experienced in communism.

In this approach, money moves from the government and, through various means, gets recycled back to them, which helps to give them more control and power and ultimately morphs them into a new world order, now known as the great reset. Back then, they discussed a one-world currency too.

Within this context, a new unconventional war was proposed in the pursuit of one-world governance, whose echoes found their way into Prince Charles's speech, and it has more to do with eliminating life than enhancing human lives.

It involves the Council of Foreign Relations, and The Club of Rome, who seek to express this ideology, and everything we are witnessing today is coming out of that playbook. I will return to this shortly. Within this historical context, we now look at a process called GeoEngineering.

Britannica defines geoengineering as‘the large-scale manipulation of a specific process central to controlling Earth’s climate for the purpose of obtaining a specific benefit.’

Solar radiation is a key influencing factor in how much is absorbed by the earth and reflected into space. The earth’s surface, cloud formation, and gases in the air are all dynamics in this process. Solar radiation management as a core theme of this process means a combination of technologies would need to be created and managed for this to happen.

Few would deny that our earth needs to be taken care of in a much more responsible way. I recall watching a documentary called A Plastic Ocean years ago, in which it was plain to see that our oceans are polluted due to human neglect.

The industrial revolution saw an increase in certain gas emissions and air pollution by corporate giants far beyond what any one individual could emit, but does the climate agenda change amount to such an issue of significant human neglect that it now requires geoengineering to correct the imbalance?

Collectively harm has been caused to the earth, so one could understand the corrective application of technology to restore balance to the earth’s ecosystem. However, in light of the findings of The Creature from Jekyll Island, it is necessary to probe further as to whether geoengineering is being deployed for a benefit or otherwise.

There is a data-rich website specifically dedicated to examining this question and the core related issues, and recently a powerful documentary was released called The Dimming.

The Dimming documentary examines weather modification through the dimming of the sun and looks at its implications for survival and living. It also examines the driving motivation behind geoengineering.

It scrutinises the extent to which geoengineers are experimenting with nature’s life support systems and examines whether they have considered the adverse effects of their methodology. In this documentary, certain things are debunked, namely:

1) Geoengineering as an experiment on the populous for nefarious reasons is a conspiracy theory.

2) The trails people witness in the sky are simply condensation trails and not artificial trails, which the layman calls chemtrails.

The documentary reveals vital point-to-point data extracted from cloud layers and other research and discovered:

1. A list of patents supporting geoengineering that goes back by at least 100 years.

2. Planes and aircraft are designed and fitted with nozzles for the express purpose of solar radiation management and the emission of chemicals into the sky to dim the sun.

3. Verification of trails that are not condensation trails, as we have been officially told, but emissions that cause artificial cloud formations designed to dim the sun and alter the ionosphere, resulting in weather modification.

4. Significant levels of aluminium in the cloud layers, which, when transmitted through nanotechnology, can get through the blood-brain barrier to cause serious illnesses such as dementia.

5. Methane deposits and craters pose an even greater threat than carbon dioxide over time.

6. The motive of military weather control by 2025.

The key objective of leading geoengineers, supported by government and military intervention, is to put 10-20 million tonnes of nanoparticles infused with certain chemicals into the sky on an annual basis.

Geoengineer and author David Keith argues for this necessity of emitting chemicals to dim the sun and cool the planet. He also adds that hundreds of thousands will die in this cause, and he sees no ‘moral hazard’ in this – this is the collateral damage we must accept for the greater good. He uses competitive language, such as winners and losers, suggesting this is not really about collaboration.

If you look at what is happening through four significant elements which form part of the building blocks of life, you will notice how the welfare of humanity is under assault from all angles.

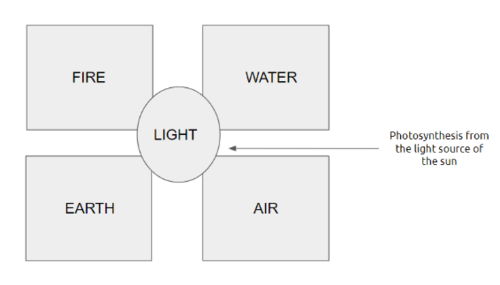

For example, the blocking of the sun has implications for the life-enhancing process of photosynthesis. Clean air and water are needed to sustain all life forms. The earth and its soil layers determine forest and plant growth.

To expand your research into geoengineering and forest fires, view this PDF called ‘Forest Fire as a Military Weapon.’ More recently, this article exposed the probable cause of the so-called forest wildfires in California in 2017. To explore the water element of flash flooding, watch this video.

An example of the overall impact on Earth and forestation can be viewed in this video. Aside from the artificial cloud formations, hurricanes provide another perspective of geoengineering processes in action through the air.

Each natural element and area is connected and impacts another in this giant ecosystem. Is geoengineering behind why bees are now falling out of the sky, and plankton are dying?

The domino effect of current geoengineering is described in the documentary. On the one hand, sulphuric acid is released from aircraft to deplete the ozone layer. Combine that with the release of aluminium, barium, strontium, and manganese, which are manipulated by high radio and microwave frequencies to alter the ionosphere, which then alters weather patterns.

One consequential scenario is where warm water goes where it should not go. Methane deposits get released from frozen players in places like the Siberian tundra and rise into the air.

Over a 10-year period, the accumulation of methane in the air is said to be at least 100 times more potent than carbon dioxide. There is evidence of methane blowouts in certain parts of the globe that look like massive craters.

Our documentarists discovered that there is enough methane in these deposits to turn our planet into Venus several times over. This is reportedly being covered up. If this is true, it means a far more serious situation has been created by geoengineering.

It is one thing to err and go off balance and then to correct a course of action. It is quite another to allow it to descend to incompetence or, worse still, corruption if deliberately intended.

At best, the powers that be have gone too far, and instead of pulling back and finding a balance between risk and reward, they are now accelerating the very problem they say they are trying to avert. Life in all its forms is under assault.

The conclusion from the documentary is that the consideration of adverse effects has not just been omitted – it has been overridden. This has not happened by accident but by design, and now we have a more serious climate problem as a result of the current agenda of geoengineering.

The many patents reveal that this has been planned for a long time and that the reduction rather than the welfare of humanity is uppermost in mind. Recall that this is something Bill Gates has heavily invested in, and the trail of money is revealing in itself.

Furthermore, the military has a clear objective and plan to ‘own’ the weather by 2025. Why such extreme measures? The common argument is that it is for defence reasons. So who or what is the enemy?

From this documentary alone, the sun is a focal point of attack in the geoengineering process, and humanity, not including themselves, is deemed to be the causative agent in the demise of the climate.

FROM GEOENGINEERING to ENGINEERING

What has become clear not just from this documentary but from the declassified information concerning covid 19 is that the strategy of ‘gain of function’ has been applied with military precision to natural assets and that humanity is not simply potential collateral damage for the greater good.

To bring this point home, let’s now return to the book, The Creature from Jekyll Island, where non-conventional forms of war were discussed to weaken the natural immune systems of the economy and life itself in order to give way to a new world order.

The Iron Report 0f 1966:

The report From Iron Mountain documents the discussions of a think tank group focussing on new and alternative war-type mechanisms by which they could achieve their agenda and strengthen government while subjugating the masses to their plan.

Many of its participants belong to the Club of Rome and/or the Council of Foreign Relations. Various real or imaginary fear-inducing global threats were discussed, such as extreme poverty, alien invasion, and poisoning the environment.

The citations below summarise their strategic thinking:-

This is what Jacques Cousteau’s had to say in his interview with the United Nations in 1991:

“Should we eliminate suffering diseases? The idea is beautiful but perhaps not beneficial for the long term….In order to stabilise world population, we must eliminate 350,000 per day.”

The Club of Rome concluded that the fear of environmental disaster would be an appropriate substitute for conventional war, and Bertrand Russell echoes this.

“War, as I remarked a moment ago, has hitherto been disappointing in this respect, but perhaps bacteriological war may prove more effective. If a Black Death could be spread throughout the world once in every generation, survivors could procreate freely without making the world too full..”

The First Global Revolution report in 1991 extends this theme further;

“In searching for a new enemy to unite us, we came up with the idea that pollution, the threat of global warming, water shortages, famine, and the like would fit the bill… All these dangers are caused by human intervention…The real enemy, then, is humanity itself.”

Whatever you think of this report, and no matter which angles you view it from, what is clear is that it describes what is playing out before our eyes.

You can see the same actors at work. For example, besides our governments, Bill Gates has invested heavily in the dimming of the sun, just as he has invested heavily into vaccines and stated that they should be a compulsory requirement for all. You see Klaus Schwab regularly talking about a new world order. You see the move toward a CBDC.

This is a giveaway to the totalitarian state imposed on us as part of a new world order. The 15-minute cities are just another twist of the knife, a component of that climate agenda. Psychological strategies, including fear and propaganda, with military-type interventions are being deployed, and their processes are poisoning us.

This is not simply geoengineering gone wrong but an engineered plan in which humanity is both the subject of experimentation and the intended target for the greater good of a few power-hungry groups. Money, power, and control are dominating themes in which the global powers separate themselves from humanity.

A more severe climate issue has emerged based on the fallout of geoengineering practices rather than the original issue it purported to solve.

We are dealing with an engineered climate agenda with elements of truth and massive deception. Now it is imperative to sort fact from fiction and recreate a different reality based on truth.

FROM ENGINEERING to REVERSE ENGINEERING

So what can we do with this knowledge, and how do we redress what is going on from an individual and collective standpoint? The good news is that this can be stopped, and a combination of things needs to come together for a new healthier, and peaceful reality to emerge.

The remedial viewpoint would be to do your own research and do everything you can to strengthen your immune system, including growing your own food. The geoengineering website has many awareness-raising materials and community action plans to tackle the various issues.

However, for long-term results and to reverse engineer the impact of the damage sustained so far, I agree with the documentary's conclusion, which relays that lasting change has to be an inside-out approach.

Start by clarifying the objective and work back from that – this is the essence of reverse engineering. What’s worse than the agenda being laid out before us is a scenario where humanity remains paralysed by fear and does nothing to change things.

What is more empowering than the prevailing agenda is that humanity awakens, not simply to what is going on, but awakens to their true core nature, so they can rise above the fears of current reality to imprint and create something new on a practical front.

Here are some tips on how to get out of neutral gear and mobilise accordingly:-

TIPS

1. Revisit the natural laws of the universe and re-evaluate your partnerships with people and the things around you. How strong and harmonious are they? Adjust your alignment accordingly.

2. Research those who are void of conflicts of interest in order to move toward truthful reporting.

3. Use Vandana Shiva’s book on Oneness v The One Percent to develop a framework of action so you can become an Ecopreneur, not just an Entrepreneur.

4. Know yourself, meaning grasp your true potential and the power of your mind. The other side knows and executes this well, albeit for detrimental effect.

5. Adjust your attitude and create better experiences. For example, if you pick litter up from the ground, do so because you care about mother earth and not simply to correct someone else's neglect. One creates an experience of genuine care and gratitude, and the other can create an experience of irritation and resentment. You choose.

6. Know that every action you take, whether individual or collective, counts. That certainty will create its own 100th Monkey Effect.

7. Be willing to share your gifts and resources, no matter how small or big. Spontaneous acts of kindness create a true community, spreading like positive wildfire and spreading light that will dispel any darkness.

It's time for the Ecopreneur to rise!

About: Anita Narayan. (United Kingdom) My life's work is about helping individuals to greater freedom through joy and purpose without self-sabotage, so that inspirational legacy can serve generations to come. Find me at my Markethive Profile Page | My Twitter Account | and my LinkedIn Profile.

Gold posts first loss in three months, but markets focus on Fed's 'hawkish pause'

The gold market posted its first monthly loss since February, wrapping May down about $36. As markets eye the crucial Congress vote to lift the debt ceiling, some Federal Reserve speakers are pushing for a "hawkish pause" at the June 13-14 meeting.

The House of Representatives is set to vote on a bill to lift the $31.4 trillion debt limit on Wednesday – a critical step to avoid a default before the June 5 deadline provided by U.S. Treasury Secretary Janet Yellen. Voting is said to start late afternoon and end before 9 pm ET time.

"The far wings of both parties are expected to show some resistance, but this bill is expected to advance," said OANDA senior market analyst Edward Moya. "The Senate might have some difficulty passing the bill, but expectations are elevated that the U.S. will avoid defaulting on its debt."

For gold, a debt deal does not necessarily mean lower prices, Moya said in a note Wednesday. "The details behind the proposed piece of legislation include significantly lower spending, which will be a major blow to the economic outlook and likely trigger a much harder-hitting recession," he noted.

The more significant risk to the gold price is what the Fed decides to do in June and July, with market expectations shifting drastically in the last few weeks.

At the time of writing, the CME FedWatch Tool was back to projecting a 70% chance of a pause at the June meeting. The market leaned towards another 25-basis-point hike only a few trading sessions ago.

U.S. rate futures also started to price in a 70% chance of a pause by the Fed Wednesday, which is a u-turn from earlier in the session, according to Refinitiv's FedWatch.

Fed speakers trigger re-pricing

Expectations shifted after several Fed speakers leaned towards pausing or skipping a rate hike in June, which is a reversal from previous hawkish sentiments.

Philadelphia Fed President Patrick Harker said Wednesday that he supports a "skip" in rate hikes.

"I am in the camp increasingly coming into this meeting thinking that we really should skip," Harker said. But Friday's employment data "may change my mind," he added.

Fed Governor and vice chair nominee Philip Jefferson also said skipping a rate hike makes sense because it gives policymakers time to examine more data.

"Skipping a rate hike at a coming meeting would allow the (Federal Open Market) Committee to see more data before making decisions about the extent of additional policy firming," Jefferson said at a financial stability conference in Washington.

But not all Fed officials share this view. Federal Reserve Bank of Cleveland President Loretta Mester said no "compelling" evidence exists not to raise rates. "I don't really see a compelling reason to pause," Mester told Financial Times in an interview Wednesday. "I would see more of a compelling case for bringing the rates up and then holding for a while until you get less uncertain about where the economy is going."

In the meantime, macro data releases have supported more tightening by the U.S. central bank. The Federal Reserve's preferred inflation measure — the annual core PCE price index — accelerated to 4.7% in April versus the consensus forecast of 4.6%.

And the latest JOLTS job openings data showed that the labor market remains tight.

All eyes are on the U.S. April nonfarm payrolls report, scheduled to be published on Friday. "Market calls that the Fed is done hiking won't be able to shake off this labor market strength if Friday's NFP report confirms this trend," Moya said.

Despite gold's failure to maintain its gains after testing record highs earlier in May, analysts say it is a good sign that gold can trade above $1,950 an ounce. But the risk of falling back to the $1,900 remains, said Kinesis Money market analyst Rupert Rowling.

"Assuming the U.S. does ratify its new debt ceiling agreement, then June looks set to be a more challenging month for gold with more bearish factors than bullish ones," Rowling said Wednesday. "Attention will quickly switch to the U.S. jobs data and then the inflation data that comes out before the Federal Reserve meets to decide its June interest rate decision in the middle of the month."

At the time of writing, August Comex gold futures were trading at $1,981.20, up 0.21% on the day.

Gold prices are solidly higher in midday U.S. trading Tuesday, supported by a weaker U.S. dollar index and a downtick in U.S. Treasury yields to start the U.S. trading week. The yellow metal hit a nine-week low overnight. Short covering in the futures market and some bargain buying in the cash were also featured today. August gold was last up $17.10 at $1,980.20 and July silver was down $0.015 at $23.34.

Trader and investor attitudes are more upbeat this week. Republican and Democratic leaders have agreed upon a deal to raise the U.S. government's debt limit. House and Senate votes on the matter are likely to occur later this week.

Asian and European stock markets were mostly firmer overnight. U.S. stock indexes are mixed to firmer at midday.

The World Gold Council reported its survey shows 24% of central banks intend to increase their gold holdings in 2023. Reasons include higher inflation, geopolitical turmoil and interest rate worries.

Gold price trades below $1,950 ahead of Congress debt ceiling vote and June Fed decision

The key outside markets today see the U.S. dollar index down on a corrective pullback after hitting a two-month high last week. Nymex crude oil prices are solidly lower and trading around $69.50 a barrel. Meantime, the benchmark 10-year U.S. Treasury note yield is presently fetching 3.702%.

Technically, August gold futures prices hit a nine-week low early on today and then rebounded to score a bullish "outside day" up. Bulls have the slight overall near-term technical advantage. However, prices are in a four-week-old downtrend on the daily bar chart. Bulls' next upside price objective is to produce a close above solid resistance at $2,000.00. Bears' next near-term downside price objective is pushing futures prices below solid technical support at $1,900.00. First resistance is seen at $1,985.00 and then at $2,000.00. First support is seen at $1,965.00 and then at today's low of $1,949.60. Wyckoff's Market Rating: 5.5

July silver futures prices hit a nine-week low Friday. The silver bears have the overall near-term technical advantage. Prices are in a four-week-old downtrend on the daily bar chart. Silver bulls' next upside price objective is closing prices above solid technical resistance at $25.00. The next downside price objective for the bears is closing prices below solid support at $22.00. First resistance is seen at today's high of $23.51 and then at $23.75. Next support is seen at $23.00 and then at the May low of $22.785. Wyckoff's Market Rating: 4.0.

July N.Y. copper closed down 160 points at 366.60 cents today. Prices closed near mid-range. The copper bears have the overall near-term technical advantage. Prices are in a six-week-old downtrend on the daily bar chart. Copper bulls' next upside price objective is pushing and closing prices above solid technical resistance at 385.00 cents. The next downside price objective for the bears is closing prices below solid technical support at 335.00 cents. First resistance is seen at today's high of 371.10 cents and then at 375.00 cents. First support is seen at today's low of 362.70 cents and then at 360.00 cents. Wyckoff's Market Rating: 3.5.

Hold gold, but hope it doesn't go up – Dominic Frisby

The key argument for gold is insurance, said Dominic Frisby, author of FlyingFrisby.com.

On May 6, 2023, Frisby spoke to Kitco at Deutsche Goldmesse in Frankfurt, Germany.

Frisby gave the rationale for gold.

"I'm a big believer in the maximum of putting five or ten percent of your net worth in gold and then hoping it doesn't go up," said Frisby, noting the metal's longevity as a store of value. "The instinct for gold is the most deep-rooted commercial instinct in the human race. In a nutshell, that is why you should own gold: because there is a permanence to it that no other substance has."

Frisby said gold does best when trust in the system is low, noting heightened culture wars and other conflicts.

"Financial crises seem to get more frequent," said Frisby. "You can just feel trust in the system generally eroding."

Frisby is a fan of Bitcoin and believes investors should hold both.

"There's a real generational divide between gold and Bitcoin," said Frisby. "Bitcoin has proved to be the most fantastic educational tool. It has educated people about fiat money and the nature of money."

Coverage of Deutsche Goldmesse 2023 sponsored by Defiance Silver.vid

'How many banks are going to need to fail?' – Matterhorn's Matthew Piepenburg on financial contagion

Stablecoins: The Anchors in the Storm of the Global Economic Crisis

The global economic landscape is undergoing a remarkable transformation as the winds of change sweep across borders and the concept of de-dollarization takes center stage. De-dollarization, a term that has gained significant traction in recent years, signifies a paradigm shift aimed at reducing the reliance on the U.S. dollar in international transactions. This phenomenon has captured the attention of economists, policymakers, and financial experts worldwide, heralding a potentially seismic shift in the global economic order.

A confluence of factors has fueled the momentum behind de-dollarization. Geopolitical tensions, trade wars, and the ascent of emerging economic powers have all played instrumental roles in reshaping the global economic climate. In the face of these multifaceted challenges, an intriguing alternative has emerged – stablecoins. These digital currencies, designed to maintain a stable value and minimize the volatility associated with traditional cryptocurrencies, have garnered considerable attention and are poised to disrupt the prevailing financial status quo.

This article aims to delve deep into the concept of stablecoins and elucidate their relevance in the context of de-dollarization. We will explore stablecoins comprehensively, and their potential implications for the global economic landscape. By shedding light on stablecoins and their intricate relationship with de-dollarization, this article aims to provide readers with a nuanced understanding of this fascinating development and its potential ramifications.

Historical Background: The Rise of Stablecoins

We can trace the rise of stablecoins as a significant player in digital currencies back to the early years of cryptocurrency development. While the concept of stable value digital currencies has existed for decades, the advent of Bitcoin in 2009 sparked a revolution in the financial world and laid the foundation for stablecoins to emerge.

In the early days of cryptocurrencies, Bitcoin gained attention for its decentralized nature and potential as a peer-to-peer electronic cash system. However, its extreme price volatility hindered its practical use as a medium of exchange and store of value. Bitcoin's value fluctuated wildly, often experiencing significant price swings within short periods.

Recognizing this volatility as a significant barrier to mainstream adoption, developers, and innovators in cryptocurrency began to explore ways to create digital assets that maintained a stable value. Their goal was to bridge the gap between the advantages of cryptocurrencies, such as efficiency and borderless transactions, with the stability of traditional fiat currencies.

The first stablecoin, Tether (USDT), was introduced in 2014 to address this issue. Tether value was pegged to the U.S. dollar on a 1:1 ratio, providing stability and liquidity for cryptocurrency traders. Despite its controversies and regulatory scrutiny in subsequent years, Tether laid the groundwork for stablecoins and demonstrated the demand for digital assets with stable values.

As the cryptocurrency market matured, stablecoins gained traction, leading to the development of alternative types of stablecoins beyond fiat-collateralized ones. One notable development was the introduction of commodity-backed stablecoins. These stablecoins were designed to be backed by tangible assets like gold or oil, providing stability through the inherent value and strength of the underlying commodities.

Another type of stablecoin that emerged was algorithmic stablecoins. These stablecoins utilized complex algorithms and smart contracts to maintain their value stability. By automatically adjusting the supply and demand dynamics, algorithmic stablecoins aimed to achieve stability without needing direct collateralization.

The popularity and adoption of stablecoins expanded significantly in 2019, especially during periods of market volatility. Stablecoins offered a refuge for traders and investors seeking to preserve the value of their assets during market downturns. Their stability and liquidity made them an attractive alternative to holding traditional fiat currencies in uncertain economic conditions.

The concept of stablecoins gained further momentum with the rapid development of blockchain technology and the rise of decentralized finance (DeFi). Stablecoins became an integral part of the DeFi ecosystem, providing a stable and reliable medium of exchange, collateral, and liquidity in decentralized lending, borrowing, and trading platforms.

Today, stablecoins continue to evolve and diversify, with many projects and protocols entering the market. Governments and central banks have also started exploring the potential of central bank digital currencies (CBDCs) as a form of stablecoin, aiming to leverage the benefits of blockchain technology while maintaining control over monetary policy.

The historical background of the rise of stablecoins showcases the ongoing quest for stability in digital currencies. From the early days of Bitcoin to the present era of DeFi and CBDCs, stablecoins have emerged as a promising solution to address the volatility inherent in cryptocurrencies. With each passing year, their relevance and importance in reshaping the global financial landscape continue to grow, making stablecoins a fascinating phenomenon to observe and explore.

De-dollarization, a trend gaining momentum in various parts of the world, is driven by geopolitical tensions, trade wars, and the rise of new economic powers. Countries like China, Russia, and Iran have been actively reducing their dependence on the U.S. dollar in international transactions, and this trend is expected to continue in the coming years. It will potentially have an impact on the stability of stablecoin.

The implications of de-dollarization for stablecoins and the broader crypto market appear chaotic at first glance. As the use of the U.S. dollar declines, demand for stablecoins pegged to the U.S. dollar, such as Tether (USDT) and USD Coin (USDC), may decrease. This shift in demand could create opportunities for alternative stablecoins pegged to other major currencies like the euro, yen, and yuan.

According to Bloomberg, the Chinese yuan surpassed the U.S. dollar as China's most popular cross-border currency, rising to a high of 48% of transactions from a low of almost 0% in 2010. This is an illustration of the de-dollarization process in operation.

If the U.S. dollar loses its dominance as the global reserve currency, stablecoins pegged to the dollar would also lose their value and stability. To address this issue, there is a need for new stablecoin legislation to bolster the U.S. dollar. The Circle founder has suggested that Congress pass new stablecoin legislation to strengthen the greenback and prevent de-dollarisation's adverse effects on stablecoins. However, some experts argue that weaponizing the dollar will destroy its reserve currency status, leading to a further rise in de-dollarization

Stablecoins can revolutionize how we conduct financial transactions, particularly in the context of de-dollarization. They can provide a secure and stable means of conducting cross-border transactions, investments, and hedging against currency fluctuations. However, governments must address several regulatory challenges and opportunities to ensure widespread adoption.

The future of U.S. pegged stablecoin will depend on several factors, including the continued dominance of the U.S. dollar in the global economy, the development of stablecoin regulations, and the ability of stablecoin to adapt to changing market conditions.

According to CoinMarketCap, every stablecoin with a market cap exceeding $1 billion is pegged to the U.S. dollar, which suggests that stablecoin's success is closely tied to the strength of the U.S. dollar. However, as de-dollarization continues to gain momentum, stablecoin may need to explore alternative pegs to maintain its stability and relevance in the market.

Stablecoins can be created in a variety of methods, but the ones that are currently in use are exogenous (backed by assets from outside the stablecoin's ecosystem) and fully/over-collateralized. Moving away from U.S. pegged stablecoins may likely not result in liquidity problems as long as the stablecoins have enough collateral, especially when a large amount of the collateral is held as highly liquid assets.

Several stablecoin projects are already addressing the challenges of de-dollarization and enhancing financial inclusion. One example is the Stellar network, which uses its native stablecoin, Lumens (XLM), to facilitate cross-border transactions and provide low-cost remittance services. Another example is the MakerDAO project, which uses its stablecoin, Dai (DAI), to provide a stable store of value that is not subject to the volatility of other cryptocurrencies.

Regulatory Challenges

Stablecoins are still largely unregulated, and concerns about their potential impact on financial stability and consumer protection exist. Regulators around the world are grappling with how to regulate stablecoins. This is a concern since stablecoins are very different from conventional crypto. Stablecoins cannot survive as they do without special national regulations. Regulation is a highly jurisdictional issue since, as we can see, crypto laws do vary slightly in different countries.

In the U.S., stablecoin regulation could be more explicit, but the SEC needs to make that happen. The United States may be delaying their response because they intend to release the digital dollar. Additionally, several organizations, including the Commodity Futures Trading Commission (CFTC), the Office of the Comptroller of the Currency (OOC), and the Financial Crimes Enforcement Network (FinCEN), must apply their own federal rules to stablecoins. In addition to federal requirements, states may have their own rules, further complicating the situation.

Japan has been seeking to regulate cryptocurrencies uniformly. However, because of their peculiar character, stablecoins are expected to undergo special regulation, much as the nation may not even regulate the U.S. dollar-pegged Stablecoins as cryptocurrencies; instead, laws may be based on the real asset they are backed by.

In a developed nation like Singapore, stablecoins are said to comply with legal requirements if the Securities and Futures Act (SFA) is applicable. Before creating a stablecoin there, one must take caution because they come under such regulations. The digital asset shouldn't have any issues functioning in the Singaporean economy if it can comply with certain regulations.

Regarding stablecoin regulation and cryptocurrency in general, Russia has been highly erratic. The nation declares that particular "digital rights" laws put out by the government in 2019 must be followed by crypto-related crowdfunding platforms and projects. Stablecoins are not specifically mentioned in this law; thus, it is reasonable to presume that the same restrictions apply to assets backed by fiat as well.

General Guidelines Regarding Stablecoin Regulation

You are now aware of the many regulations that apply to stablecoins. But because cryptocurrencies are a worldwide commodity, it's critical to recognize the global legislation parallels. Fiat-backed currencies, for example, all plainly emphasize the transfer of value. Therefore, governments will need to ensure that parties may use stablecoins without risk. To prevent these transactions from being utilized for tax avoidance, they will also need to declare them.

The issue of what to do with the stablecoins follows. Some people could utilize them to send money overseas for payments. Others could view them as an alternate means of holding and investing in commodities like gold. Finally, these nations must consider global stablecoin law. In other words, they should observe how other countries accomplish the goals they seek to achieve. Authorities must also discuss if a single worldwide regulatory approach is preferable to several separate ones.

Stablecoins have emerged as an alternative to traditional currencies, offering stability, security, and transparency. In the context of de-dollarization, stablecoins have the potential to play a significant role in navigating the future of the global economy. However, several regulatory challenges and opportunities must be addressed to ensure widespread adoption. As the world shifts away from the U.S. dollar, stablecoins will become increasingly relevant, providing a secure and stable means of conducting cross-border transactions, investments, and hedging against currency fluctuations.

This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

About: Prince Ibenne. (Nigeria) Prince is passionate about helping people understand the crypto-verse through his easily digestible articles. He is an enthusiastic supporter of blockchain technology and cryptocurrency. Find me at my Markethive Profile Page | My Twitter Account | and my LinkedIn Profile.

Top 10 Cybercurrency Wallets: What They Are and How to Use Them

Cryptocurrency wallets are digital wallets that store and manage a user's private and public keys used to access their cryptocurrency. These wallets enable users to send and receive digital currency and monitor their balance. Unlike traditional wallets, cryptocurrency wallets are not backed by government deposit schemes, and they only hold digital currencies. There are two main types of cryptocurrency wallets: hot wallets and cold wallets. Hot wallets are connected to the internet and are more accessible, while cold wallets are offline and more secure.

Using a cryptocurrency wallet is relatively easy, but it is essential to understand the different types and how they work. A user must first choose a wallet that supports the specific cryptocurrency they want to store. Then, they need to download and install the wallet software or sign up for a web-based wallet service. Once the wallet is set up, the user can send and receive cryptocurrency by sharing their wallet address with others. It is crucial to keep the private keys secure and not share them with anyone, as this can lead to theft of the cryptocurrency.

There are many cryptocurrency wallets available, each with different features and levels of security. Some of the top wallets include Ledger Nano S, Trezor, and Exodus. It is essential to research and compare different wallets before choosing one to ensure the wallet meets the user's needs and offers the necessary security.

What Are Cybercurrency Wallets?

Overview

A cybercurrency wallet is a digital wallet that stores a user's cryptocurrencies. It is a software program that interacts with the blockchain to enable users to send and receive digital currency and monitor their balance. Cryptocurrency wallets do not physically hold cryptocurrencies, but instead, they store the private and public keys that allow users to access and manage their digital assets.

Types of Cybercurrency Wallets

There are several types of cybercurrency wallets available, each with its unique features and security measures. The two main categories of cybercurrency wallets are hardware wallets and software wallets.

Hardware Wallets

Hardware wallets are physical devices that store a user's private keys offline, making them less susceptible to hacking or theft. They are considered the most secure type of cybercurrency wallet. Hardware wallets can be further categorized into cold wallets and hot wallets.

Cold Wallets: Cold wallets are hardware wallets that are not connected to the internet, making them immune to hacking attempts. They are ideal for storing large amounts of cryptocurrency for an extended period.

Hot Wallets: Hot wallets are hardware wallets that are connected to the internet, making them more vulnerable to hacking attempts. They are ideal for storing small amounts of cryptocurrency for everyday use.

Software Wallets

Software wallets are digital wallets that run on a computer or mobile device. They are categorized into desktop wallets, mobile wallets, and web wallets.

Desktop Wallets: Desktop wallets are software wallets that are installed on a computer. They offer more security than web wallets but are still vulnerable to hacking attempts.

Mobile Wallets: Mobile wallets are software wallets that run on a mobile device. They offer convenience and portability but are less secure than desktop wallets.

Web Wallets: Web wallets are software wallets that run on a web browser. They are the least secure type of cybercurrency wallet as they are vulnerable to hacking attempts and phishing attacks.

In conclusion, cybercurrency wallets are essential tools for managing and securing digital assets. It is crucial to choose a wallet that suits your needs and offers the necessary security measures to protect your cryptocurrencies.

How to Use Cybercurrency Wallets

Cybercurrency wallets are essential tools for managing cryptocurrencies. They allow users to store, send, and receive digital assets such as Bitcoin, Ethereum, and other tokens. In this section, we will discuss how to use cybercurrency wallets effectively.

Setting Up a Cybercurrency Wallet

To use a cybercurrency wallet, you must first set it up. The process varies depending on the wallet you choose, but generally, you will need to follow these steps:

Download the wallet software or app from the official website or app store.

Create a new wallet account by providing your email address and creating a strong password.

Generate a seed phrase, which is a series of words that can be used to recover your wallet if you lose your password or device.

Save your seed phrase in a secure place, such as a password manager or a physical document.

Set up two-factor authentication to add an extra layer of security to your account.

Sending and Receiving Cryptocurrencies

Once you have set up your wallet, you can start sending and receiving cryptocurrencies. To send crypto transactions, you will need to follow these steps:

Log in to your wallet and navigate to the send section.

Enter the recipient's public key or wallet address.

Enter the amount of cryptocurrency you want to send.

Review the transaction details and confirm the transaction.

To receive crypto transactions, you will need to provide your public key or wallet address to the sender. They can then send the desired amount of cryptocurrency to your wallet.

Managing Transactions

Cybercurrency wallets allow you to manage your transactions effectively. You can view your transaction history, track your balance, and manage your wallet settings. To manage your transactions, you will need to follow these steps:

Log in to your wallet and navigate to the transactions section.

View your transaction history and filter by date, amount, or type.

Check your balance and monitor your wallet's performance.

Adjust your wallet settings, such as transaction fees or privacy settings, as needed.

In conclusion, cybercurrency wallets are powerful tools for managing cryptocurrencies. By following the steps outlined in this section, you can set up, send, and receive cryptocurrencies with ease. Remember to always prioritize security by using strong passwords, two-factor authentication, and secure storage methods for your seed phrase.

Top 10 Cybercurrency Wallets

When it comes to storing cryptocurrencies, having a reliable wallet is crucial. There are various types of wallets available, including hardware wallets, software wallets, desktop wallets, mobile wallets, web wallets, online wallets, custodial wallets, and non-custodial wallets. In this section, we will discuss the top 10 cybercurrency wallets that are trusted by many users.

Ledger Nano S

Ledger Nano S is a hardware wallet that provides a secure way to store cryptocurrencies. It supports over 1,500 cryptocurrencies and is compatible with Windows, Linux, and Mac operating systems. It features a small screen that displays transaction details, and users can confirm transactions by pressing physical buttons on the device.

Trezor

Trezor is another hardware wallet that is known for its security features. It supports over 1,000 cryptocurrencies and is compatible with Windows, Linux, and Mac operating systems. It features a small screen that displays transaction details, and users can confirm transactions by pressing physical buttons on the device.

Exodus

Exodus is a software wallet that is available for desktop and mobile devices. It supports over 100 cryptocurrencies and allows users to exchange cryptocurrencies within the wallet. It also features a built-in portfolio tracker that displays the value of the user's assets.

MetaMask

MetaMask is a web wallet that is compatible with various web browsers, including Google Chrome, Firefox, and Brave. It supports Ethereum and other ERC-20 tokens and allows users to interact with decentralized applications (dApps) on the Ethereum network.

Trust Wallet

Trust Wallet is a mobile wallet that is available for iOS and Android devices. It supports various cryptocurrencies and allows users to interact with dApps on the Ethereum, Binance Smart Chain, and other networks. It also features a built-in DEX (decentralized exchange) that allows users to trade cryptocurrencies within the wallet.

Coinbase Wallet

Coinbase Wallet is a mobile wallet that is available for iOS and Android devices. It supports various cryptocurrencies and allows users to interact with dApps on the Ethereum and other networks. It also features a built-in DEX that allows users to trade cryptocurrencies within the wallet.

Atomic Wallet

Atomic Wallet is a desktop and mobile wallet that supports over 500 cryptocurrencies. It features a built-in exchange that allows users to trade cryptocurrencies within the wallet. It also allows users to stake some cryptocurrencies and earn rewards.

Crypto.com Defi Wallet

Crypto.com Defi Wallet is a mobile wallet that supports various cryptocurrencies and allows users to interact with dApps on the Ethereum and Binance Smart Chain networks. It also features a built-in DEX that allows users to trade cryptocurrencies within the wallet. Users can also earn rewards by staking some cryptocurrencies.

Solana Wallet

Solana Wallet is a web wallet that supports Solana and SPL (Solana Program Library) tokens. It allows users to interact with dApps on the Solana network and features a built-in DEX that allows users to trade SPL tokens within the wallet.

Avalanche Wallet

Avalanche Wallet is a web wallet that supports Avalanche and other assets on the Avalanche network. It allows users to interact with dApps on the Avalanche network and features a built-in DEX that allows users to trade assets within the wallet.

In conclusion, these are the top 10 cybercurrency wallets that are trusted by many users. Each wallet has its own unique features and benefits, so it's important to choose the one that best suits your needs. Whether you prefer a hardware wallet, software wallet, or web wallet, there is a wallet out there that can help you store your cryptocurrencies securely.

Security Features of Cybercurrency Wallets

When it comes to cybercurrency wallets, security is a top priority. These wallets are designed to protect your digital assets from theft, fraud, and other security threats. Here are some of the security features you can expect from most cybercurrency wallets:

Private Keys

One of the most important security features of a cybercurrency wallet is the private key. This is a secret code that allows you to access your digital assets and make transactions. Your private key should never be shared with anyone else, as it is the key to your wallet.

Public Key

In addition to your private key, your wallet also has a public key. This is a code that allows others to send digital assets to your wallet. Unlike your private key, your public key can be shared with others.

Two-Factor Authentication

Many cybercurrency wallets offer two-factor authentication (2FA) as an additional security measure. This requires you to enter a code or use an app on your phone in addition to your password to access your wallet. This adds an extra layer of security to your wallet.

Seed Phrase

A seed phrase is a series of words that can be used to recover your wallet if you lose your private key. This is an important security feature, as it allows you to regain access to your digital assets if your private key is lost or stolen.

Cold Storage

Some cybercurrency wallets offer cold storage options. This means that your digital assets are stored offline, which makes them less vulnerable to hacking and other security threats. Cold storage is an excellent security feature for those who want to keep their digital assets safe for the long term.

Hot Wallets

On the other hand, hot wallets are connected to the internet and are more vulnerable to hacking and other security threats. While hot wallets are convenient for making frequent transactions, they are not as secure as cold wallets.

Third-Party Risk

When using a cybercurrency wallet, it is important to be aware of third-party risks. This includes the risk of using a wallet that is not secure, as well as the risk of using a wallet that is owned by a third party. It is important to do your research and choose a wallet that is reputable and trustworthy.

Ownership

Finally, it is important to remember that you are responsible for the security of your digital assets. This means that you should take the necessary precautions to keep your private key and other sensitive information safe. By taking the time to learn about cybercurrency wallet security features and best practices, you can help ensure that your digital assets remain safe and secure.

Cryptocurrency Wallets and Blockchain

Cryptocurrency wallets are digital wallets that allow users to store, manage, and trade their cryptocurrencies. These wallets interact with various blockchains to enable users to send and receive digital currency and monitor their balance. Blockchain is the technology that underpins cryptocurrencies, and it is a decentralized, distributed ledger that records transactions across a network of computers.

One of the benefits of blockchain technology is that it provides a high level of security. Because the ledger is distributed across many computers, it is difficult for any one person or organization to tamper with the data. This makes blockchain an ideal technology for storing and transferring value, such as cryptocurrencies.

Decentralized finance (DeFi) is a growing area of blockchain technology that aims to provide financial services in a decentralized manner. DeFi applications, or dApps, are built on top of blockchains and allow users to access financial services such as lending, borrowing, and trading without the need for intermediaries like banks.

Fungible tokens are digital assets that are interchangeable with each other, such as cryptocurrencies. Non-fungible tokens (NFTs) are unique digital assets that are not interchangeable, such as digital art or collectibles. NFTs are becoming increasingly popular, and some wallets now support the storage and trading of NFTs.

The decentralized web is another area of blockchain technology that is gaining traction. The decentralized web aims to provide a more open and decentralized internet that is not controlled by a few large corporations. Decentralized web applications are built on top of blockchains and aim to provide a more secure and private internet experience.

There are many different cryptocurrency wallets available, each with their own strengths and weaknesses. Some wallets are designed for beginners, while others offer more advanced features for experienced users. The top 10 wallets are:

Ledger Nano S

Trezor

Exodus

MyEtherWallet

Electrum

Jaxx

Coinbase Wallet

Edge

Trust Wallet

Atomic Wallet

Each of these wallets has its own unique features and benefits, and users should carefully consider their needs and preferences before choosing a wallet.

Pros and Cons of Using Cybercurrency Wallets

Cybercurrency wallets have become increasingly popular as digital currencies continue to gain traction. These wallets offer a secure and convenient way to store, manage, and transact cryptocurrencies. However, like any financial tool, there are pros and cons to using cybercurrency wallets.

Pros

Enhanced Security

One of the most significant advantages of using cybercurrency wallets is enhanced security. Unlike traditional financial accounts, cybercurrency wallets use advanced encryption algorithms to protect your funds. Additionally, many wallets offer two-factor authentication and other security features to prevent unauthorized access.

Easy to Use

Most cybercurrency wallets are designed to be user-friendly and easy to navigate. Many wallets offer intuitive interfaces, making it easy to manage your funds, send and receive payments, and view transaction history.

Lower Transaction Fees

Cybercurrency wallets typically have lower transaction fees than traditional financial accounts. This is because most wallets do not charge fees for transactions, and those that do typically charge lower fees than banks and credit card companies.

Cons

Personal Information

When you use a cybercurrency wallet, you are required to provide personal information, such as your name and address, to verify your identity. While this information is typically kept secure, there is always a risk of data breaches or other security vulnerabilities.

Credit Card and Bank Account Integration

While some cybercurrency wallets allow you to link your credit card or bank account, this can be a double-edged sword. While it may make it easier to buy and sell cryptocurrencies, it also increases the risk of fraud and identity theft.

Limited Acceptance

While cryptocurrencies have gained significant traction in recent years, they are still not widely accepted as a form of payment. This means that you may not be able to use your cybercurrency wallet to make purchases at all merchants.

Each wallet has its own unique features and benefits, so it's important to research and compare before choosing the right wallet for you.

U.S. economic data hammers gold price as markets gear up for a rate hike in June

The gold market got battered by upbeat economic data and stubbornly high inflation. As gold posted its third weekly loss, markets recalibrated for another 25-basis-point rate hike in June after pause expectations got shattered.

Gold is looking to close down $35 on the week, with June Comex gold futures last trading at $1,945.80 an ounce. Despite the selloff, year-to-date gold is still up more than 6%.

The macro data was the main driver weighing on gold at the end of the week, TD Securities global head of commodity strategy Bart Melek told Kitco News.

"The durable goods number, personal spending, and the PCE inflation measures were all broadly above expectations," Melek said. "Not only is inflation not dropping, the Federal Reserve's preferred inflation measure — the core PCE price index — went to 4.7% in April."

Inflation near 5% is too high for the Fed to justify a pause in June, and the market is pricing that in. The latest market expectations see a 60% chance of a hike at the June 13-14 meeting, Gainesville Coins precious metals expert Everett Millman told Kitco News.

"That is a big reversal from earlier estimates," he said. "The speed at which this kind of re-pricing happens gets the attention of the gold market. Rapid changes in expectations lend themselves to more volatility."

On top of that, the U.S. dollar has performed well, and gold responded with a move down. "We think gold prices may be subdued for much of the quarter and probably into the early part of Q3," Melek said. "The market has mispriced Fed's intentions."

With the Fed zeroed in on inflation, not much will likely sway the central bank before the June meeting. Millman added that the debt ceiling debate drama is the one thing to closely monitor as any downgrades to the U.S. credit rating would trigger safe-haven flows into gold.

Meanwhile, negotiations to raise the U.S. government's $31.4 trillion debt ceiling before June 1 hit some obstacles on Friday. Earlier, Democratic and Republic negotiators appeared nearing a deal to lift the debt cap for two years while limiting some spending.

"We have made progress," lead Republican negotiator Garret Graves told reporters. "I said two days ago, we had we had some progress that was made on some key issues, but I want to be clear, we continue to have major issues that we have not bridged the gap on chief among them work requirements."

Gold price levels to watch

The next support level for gold is $1,940 an ounce, Millman said. Below that, investors should watch the $1,915 and $1,900.

Analysts do not rule out a move lower to $1,900. "Firm support is at around $1,900-$1,896," Melek said.

It is too soon to call a bottom in gold even though the precious metal is down more than $125 since testing record highs a few weeks ago, RJO Futures senior market strategist Frank Cholly told Kitco News.

"The market is telling us we will see another rate hike in June and maybe one in July. Gold doesn't like that," Cholly said. "Somewhere between the $1,950-$1,925 range on August futures, traders will find value, and the market will form a base before turning higher," he said.

Data next week

Tuesday: U.S. CB consumer confidence

Wednesday: U.S. JOLTs job openings, Beige Book

Thursday: U.S. jobless claims, U.S. ADP nonfarm employment, U.S. ISM manufacturing PMI

Mycarclub: The Ultimate Destination for Car Enthusiasts

MyCarClub is a platform that brings together car enthusiasts from all over the world. The website offers a tight-knit community where members can share their love for anything on wheels. The platform provides weekly newsletters on the latest motor releases, events, exhibitions, and more. The website believes that cars aren't just machines, but a way of life. From muscle cars to exotic rides, MyCarClub is always eager to hear about the latest developments in the automotive industry.

One of the unique features of MyCarClub is that it is a reward-based private crowd-funding club. Members can qualify to drive a new car of their choice depending on the qualification criteria. Members' monthly subscriptions form a part of a pool that is used to assist others to get their reward. The monthly donations of group members are also used to help other members achieve their dream of driving their favorite car.

However, before becoming a member, it is essential to understand the rules and regulations of the platform. MyCarClub is a legitimate business, but it is always important to be cautious when joining any club or platform. Members should read the fine print carefully and understand the terms and conditions before signing up. Overall, MyCarClub offers a unique opportunity for car enthusiasts to connect with like-minded individuals and potentially drive their dream car.

MyCarClub is a car club that aims to provide its members with a unique, exclusive, and unparalleled experience. The club offers a wide range of benefits tailored to individual needs and desires, ensuring each customer has a safe and enjoyable experience that leaves them coming back for more. MyCarClub has a mission to provide its members with a chance to drive the car of their dreams while keeping the cost affordable.

The club provides members with a variety of cars to choose from, including luxury cars, sports cars, and more. Members can choose the car they want to drive and enjoy the experience of driving a car they have always dreamed of. MyCarClub also offers a range of benefits to its members, including insurance, maintenance, and cleaning services.

MyCarClub is a legitimate business that has been vetted and reviewed by Scam Detector, who gave it a medium authoritative score of 63.2. This means that the business is known, vetted, and legitimate. The club has also received positive reviews from its customers on Trustpilot, with an average rating of 3.7 out of 5.

Overall, MyCarClub is an excellent option for those who want to experience driving a luxury or sports car without breaking the bank. The club offers a range of benefits to its members, making it a great choice for car enthusiasts who want to enjoy the thrill of driving a high-end car.

Membership Benefits

Mycarclub.com offers an array of benefits to its members, making it a unique and exclusive experience. The club aims to provide each member with a safe and enjoyable experience that leaves them coming back for more. The following are some of the membership benefits:

Monthly Offers

Mycarclub offers its members monthly discounts and special offers on various products and services. These offers are exclusive to members only and can be accessed through the club's website. Members can save a significant amount of money on their purchases, making their membership fee worth it.

Events

Mycarclub organizes various events throughout the year, ranging from car shows to meet-and-greet events. These events are an excellent opportunity for members to socialize, network, and showcase their cars. Members can also participate in various competitions and win exciting prizes.

Networking

Mycarclub provides members with a platform to network with other car enthusiasts. Members can interact with each other through the club's website or social media platforms. The club also organizes networking events where members can meet and connect with like-minded people.

In conclusion, Mycarclub provides its members with an exclusive and unparalleled experience. The club offers various membership benefits, including monthly discounts, events, and networking opportunities. Members can save money, socialize, and connect with other car enthusiasts.

Customer Service and Support

Mycarclub prides itself on providing top-notch customer service and support to its members. With a focus on powerful assistance and weekly tips, members can rest assured that they are receiving the best possible support for all of their car-related needs.

Powerful Assistance

Mycarclub offers powerful assistance to its members, ensuring that they have access to the help they need when they need it. The company's customer service team is available 24/7 to assist with any issues or concerns that may arise. Members can reach out to the team via phone, email, or live chat, and can expect a prompt and helpful response.

In addition to traditional customer service channels, Mycarclub also offers a range of online resources to help members troubleshoot issues on their own. The company's website features a comprehensive FAQ section, as well as helpful articles and guides that cover a wide range of car-related topics.

Weekly Tips

Mycarclub also provides its members with weekly tips to help them stay on top of their car maintenance and care. These tips cover a range of topics, from basic maintenance tasks like oil changes and tire rotations to more advanced topics like engine repair and performance upgrades.

Members can access these tips via the company's website or through the Mycarclub mobile app. The tips are designed to be easy to understand and implement, even for those with limited car knowledge or experience.

Overall, Mycarclub customer service and support offerings are among the best in the industry. With powerful assistance and weekly tips, members can feel confident that they have the help and resources they need to keep their cars running smoothly and safely.

Owning a dream car is a goal for many people. However, the cost of purchasing a new car can be prohibitive. MyCarClub offers an innovative solution to this problem. By joining the club, members can drive their dream car for as little as $33 a month.

New Car Selection

MyCarClub offers a wide selection of new cars to choose from, including luxury brands such as BMW, Mercedes-Benz, and Audi. Members can select the car of their dreams and enjoy the thrill of driving it without the high cost of ownership.

The selection process is easy and convenient. Members can browse the website and select the car they want. Once they have made their selection, the car will be delivered to their doorstep.

Car Shows

MyCarClub also hosts car shows for members to enjoy. These shows offer an opportunity for members to see the latest models and network with other car enthusiasts.

The car shows are held at various locations across the country, making it easy for members to attend. Members can also showcase their own cars at these events and receive recognition for their unique vehicles.

In conclusion, MyCarClub offers a unique and affordable solution for dream car ownership. With a wide selection of new cars to choose from and exciting car shows to attend, members can enjoy the thrill of driving their dream car without breaking the bank.