THE ENGINE POWER OF MARKETHIVE: The Power of the Dual-Engine Strategy

Markethive, a pioneering force in market networks, has quickly become a haven for individuals seeking financial independence and freedom from oppressive systems. Its unique and comprehensive ecosystem, featuring a wide range of platforms and profitable opportunities for entrepreneurs, is experiencing rapid growth. This growth is fueled by the realization of its visionary plans through strategic integrations and innovative advancements.

In this dynamic and ever-evolving ecosystem, Markethive nurtures a community of empowered individuals who actively shape their financial destinies. By providing essential tools, resources, and infrastructure for entrepreneurial success, Markethive is democratizing access to wealth creation and paving the way for a more equitable and inclusive economic landscape.

As the Markethive network continues to expand and mature, its impact on the global economy is becoming increasingly profound. By championing the principles of financial sovereignty and individual empowerment, Markethive is not just transforming lives but also reshaping the foundations of the financial world. In the face of growing economic uncertainty and social unrest, Markethive stands as a beacon of hope, illuminating a path toward a brighter and more prosperous future for all.

The Two Primary Engines Driving Markethive's Success

Unlike many social media and online marketing platforms that depend on a single driving force for user engagement and growth, Markethive distinguishes itself by employing a dual-engine strategy to attract and retain an extensive network of entrepreneurs. This innovative approach centers on two primary mechanisms: the subscriber engine and the traffic engine. These engines collaborate to foster a dynamic and thriving online ecosystem.

- The Subscriber Engine: This engine aims to cultivate a community of registered users who actively log in and engage with the platform's content and features. Markethive encourages users to become subscribers and contribute to the platform's growth by providing valuable resources, tools, and networking opportunities. This engine resembles the model used by platforms like LinkedIn, where users are required to create an account and log in to access the complete range of services.

- The Traffic Engine: This engine focuses on attracting a steady stream of site visitors, whether registered users or not. By offering high-quality content, optimizing for search engines, and utilizing social media, Markethive creates organic traffic and broadens its reach. This engine is similar to the strategy employed by platforms like CoinTelegraph, which primarily aims to deliver news and information to a broad audience.

The Power of the Dual-Engine Strategy

By integrating the subscriber engine with the traffic engine, Markethive creates a synergistic effect that boosts its influence and accelerates its growth. The subscriber engine fosters a sense of community and loyalty among registered users, while the traffic engine ensures a continuous influx of new visitors who could become subscribers. This dual-engine strategy enables Markethive to sustain a balance between user engagement and reach, ultimately positioning it as a premier hub for entrepreneurs in the digital marketplace.

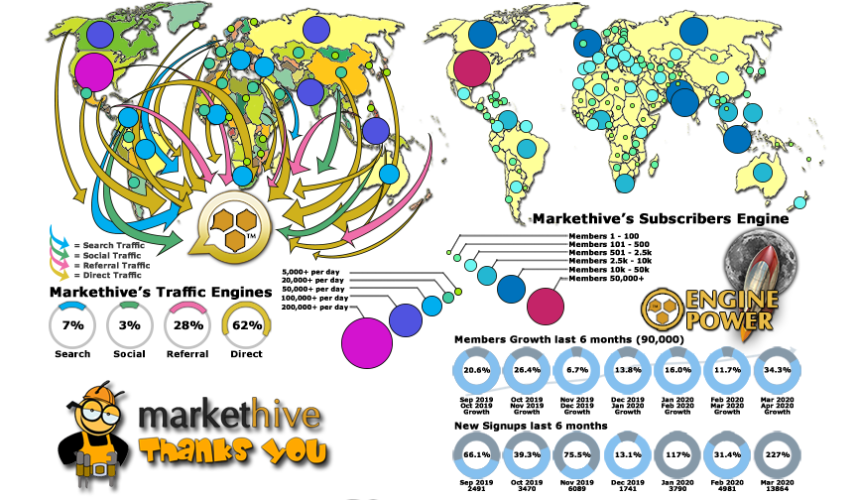

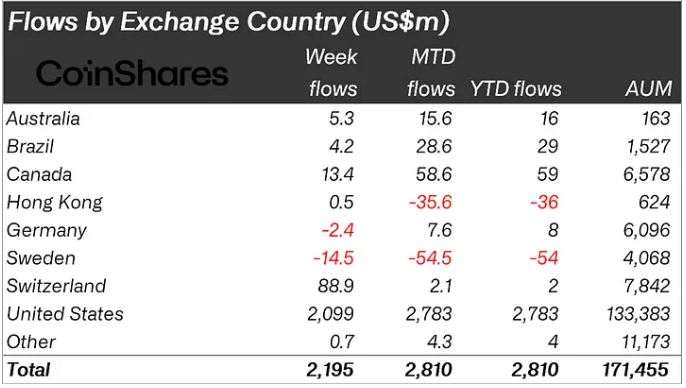

The infographic above depicts Markethive's impressive growth over a six-month period, combining internal and external statistics to illustrate the company's success.

Traffic Engine

The traffic engine data reveals the various sources contributing to Markethive's website traffic. Direct traffic from the Subscriber Engine makes up 62% of total traffic. This indicates strong user engagement and loyalty, with members frequently visiting the site directly. External referral sites represent 28% of traffic, showcasing the effectiveness of partnerships and external promotions. Search traffic accounts for 7%, illustrating the platform's visibility in search engine results. Social traffic constitutes 3% of total traffic, emphasizing the potential for further growth through social media channels.

Subscriber Engine

The Subscriber Engine data highlights the rapid growth of Markethive's user base. The platform is gaining significant momentum with a member increase of 90.8K and a 227% rise in new subscribers. Implementing strict validation measures, including OAuth, KEY, and SMS verification, guarantees the authenticity of all accounts and protects the platform's integrity.

Overall Growth Rate

The remarkable overall growth rate of 2,849% highlights Markethive's success in attracting and retaining users. A mix of factors, such as effective marketing strategies, a compelling value proposition, and positive user experiences, likely drives this significant growth.

Dynamic Growth

It's important to note that the statistics presented in the infographic are dynamic and subject to ongoing change. As Markethive continues to grow and evolve, these metrics will surely increase, reflecting the platform's continued success.

The infographic offers a compelling visualization of Markethive's rapid growth trajectory. The blend of a robust Traffic Engine and a thriving Subscriber Engine has elevated the platform to new heights, creating a strong foundation for future success. By prioritizing user engagement, innovation, and data-driven strategies, Markethive is well-positioned to maintain its impressive growth and reinforce its status as a leader in the industry.

Markethive has cultivated a diverse and inclusive global community, welcoming individuals from all corners of the world, regardless of race, creed, age, profession, or personal interests. While many social and online platforms exploit these differences to sow discord and division, Markethive embraces them as strengths, recognizing that diversity fosters a richer, more dynamic community. Our platform transcends superficial differences, focusing on shared values and aspirations.

At Markethive, we are united by a common pursuit of liberty, freedom, economic sovereignty, and entrepreneurialism. These shared ideals create a powerful bond, fostering a sense of community and collaboration among our members. This emphasis on shared values allows Markethive to emerge as a global leader for entrepreneurs, irrespective of language, religion, or nationality. By providing a platform that transcends traditional barriers, Markethive empowers entrepreneurs from all backgrounds to connect, collaborate, and succeed in the global marketplace.

Markethive Secondary Engines

In addition to these primary engines, Markethive also leverages secondary engines and smaller businesses to support its growth and expansion.

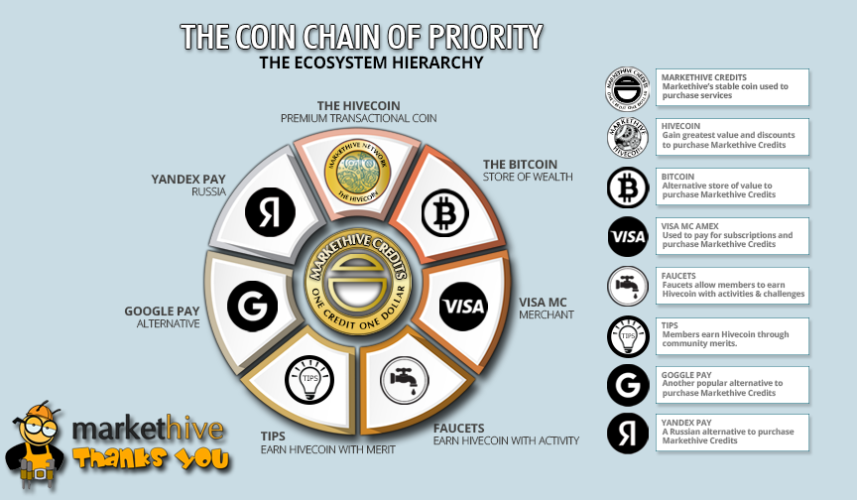

- Hivecoin, Markethive's cryptocurrency, incentivizes user engagement and facilitates transactions within the platform.

- The Exchange Engine allows users to trade Hivecoin and other cryptocurrencies, enhancing the platform's utility.

- Numerous smaller Markethive businesses contribute to the ecosystem by providing specialized services and products. These businesses work together to create a comprehensive, interconnected network that benefits all users.

By integrating these various engines, Markethive has created a robust and self-sustaining ecosystem that fosters collaboration and drives success. This interconnected system allows Markethive to reach out to other platforms and forge strategic partnerships, further expanding its reach and influence. Through this collaborative approach, Markethive can achieve its mission of empowering entrepreneurs and businesses worldwide.

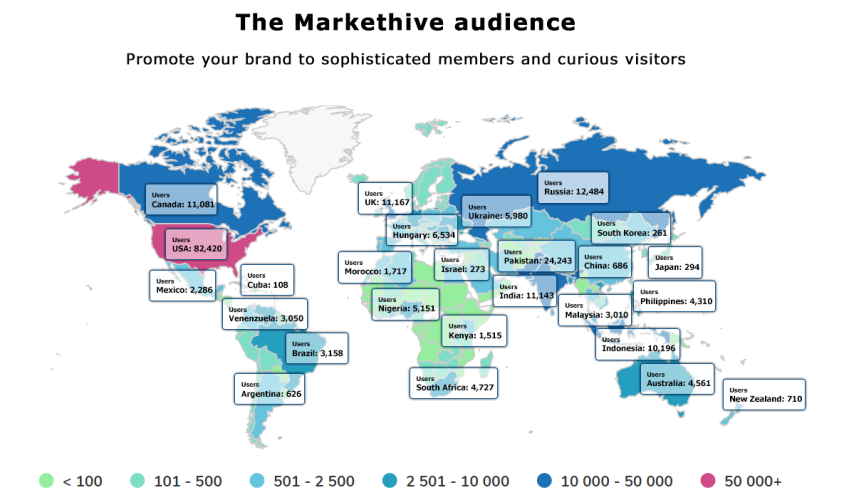

Who is the Markethive Audience?

The Markethive audience represents a valuable demographic for targeted advertising campaigns. Primarily composed of entrepreneurs, this group actively seeks resources and tools to grow their online businesses. These desirable resources include, but are not limited to, training programs, educational eBooks, live mentoring opportunities, software enhancements, SEO services, and website traffic tracking and analytics tools. This makes Markethive, along with its affiliated network of domains, a highly appealing and potentially profitable platform for third-party advertisers looking to engage with a motivated and involved audience of entrepreneurs.

Markethive is pioneering a new approach to cryptocurrency transactions and advertising. It will enable external websites and forums to integrate APIs seamlessly to conduct transactions with Hivecoin across various platforms. This innovative approach starkly contrasts existing systems that only accept other cryptocurrencies as payment. By enabling the use of Hivecoin for transactions across multiple platforms, Markethive is poised to revolutionize how businesses and individuals interact with cryptocurrency.

Hivecoin (HVC) is poised to become very popular because it represents a vertical, unique set of engines, a traffic engine, and a subscriber engine, and as Markethive subscribers are the world’s entrepreneurs, we accumulate, hold, and spend, then let the free market do the rest and watch Markethive’s utility crypto, increase in value.

.png)

Summary

Markethive distinguishes itself as a unique and comprehensive platform that merges social networking, inbound marketing capabilities, and digital media functionalities. Its integration of blockchain technology, a self-contained financial economy, and a vast array of tools and portals create a holistic ecosystem that entrepreneurs and businesses can readily adopt and leverage for growth.

Designed with a community-centric approach, Markethive empowers its users by providing a cutting-edge platform that fosters control, self-sovereignty, privacy, and autonomy. This creates an environment where individuals have a genuine opportunity to unlock their full potential, cultivate wealth, and achieve prosperity through diverse avenues.

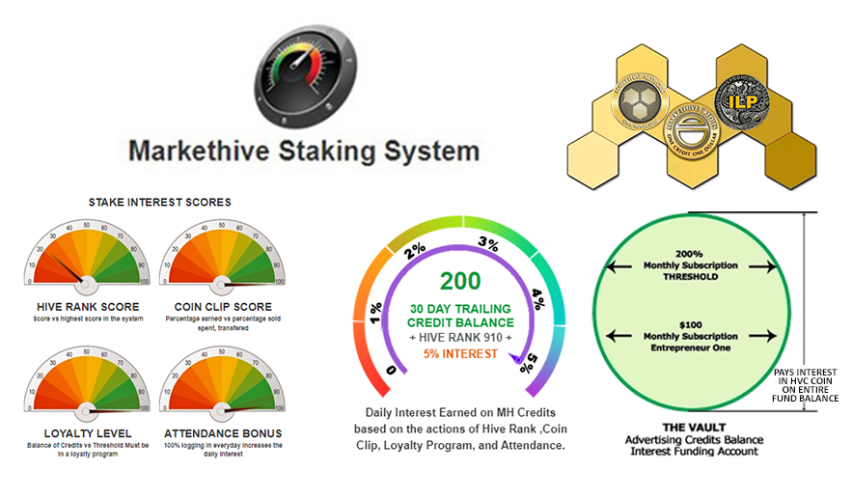

Collaboration is central to Markethive's philosophy. The platform operates with two primary engines as well as secondary engines like Markethive’s cryptocurrency, Hivecoin (HVC), its comprehensive wallet, and the Banner Impressions Exchange (with many more vertical protocols and systems in development), which facilitate seamless connections between cottage businesses within Markethive and external platforms. This interconnectedness fosters a symbiotic relationship where the success of one entity contributes to the collective prosperity of the entire network.

In essence, Markethive embodies a dynamic ecosystem where innovation, collaboration, and entrepreneurialism converge, providing a fertile ground for individuals and businesses to thrive in the digital age. By offering a comprehensive suite of tools, fostering a supportive community, and integrating cutting-edge technologies, Markethive is not merely a platform but a catalyst for success in the ever-evolving landscape of social media, marketing, and digital media. Markethive is the name, and Entrepreneurialism is the game.

.png)

Tim Moseley

.png)

.png)

.png)

.png)

.png)

%20copy.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)