The Evolution of an Ecosystem: A Rapidly Developing Technological Revolution

Evolution is fundamental to everything on our planet, whether living or non-living. In my lifetime, technology has been one of the fastest-changing fields. We’ve seen more technological advances in the past century than in all previous centuries combined, and this pace of change continues. Undoubtedly, this has led to a faster, more convenient, and to some extent, comfortable way of life. The one constant that remains, however, is the enduring presence of oligarchic monopolies, still exerting their influence, but for how long?

When used rightly for human progress, digital technology stems from divine inspiration and can serve as a powerful, positive force. Nonetheless, it has also been exploited for malicious purposes driven by greed, desire for power, and control. As with everything, technology must adapt and evolve to stay relevant. The issues arising from current technologies motivate the creation of new, opposing solutions.

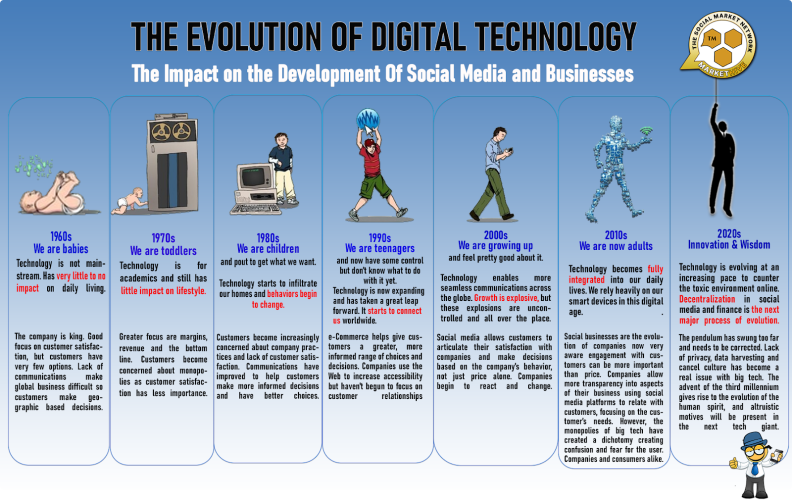

Technological innovation, notably since the advent of the Internet, has profoundly reshaped our world. Early pioneers included Yahoo (1994), a comprehensive web portal that offered search, email, and financial news, dominating the nascent digital landscape as a primary gateway, before partnering with Google. Markethive, then known as Veretekk, emerged as an automated marketing platform in 1998, introducing email autoresponders and SaaS tools to the growing digital marketing sector.

The mid-2000s saw the emergence of MySpace (2005), which tapped into human connection and self-expression, quickly becoming a global social networking phenomenon and surpassing giants like Yahoo and even Google by 2006 in terms of unique visitors. Yet, MySpace's reign, while impactful, was relatively brief. By 2009, a newer, even more expansive social network, Facebook, had globally eclipsed MySpace.

Facebook (launched in 2004) succeeded due to a cleaner interface, robust features, and aggressive international expansion, ultimately redefining online social interaction. This continuous cycle of innovation, disruption, and re-invention remains a defining and exhilarating characteristic of the technology sector, where yesterday's giants can quickly become tomorrow's footnotes, and new paradigms are constantly being forged.

Falling From Grace

In a rapidly changing global environment, organizations that become complacent or adopt a "too big to fail" mindset risk falling behind. Constant innovation through ongoing research and development is crucial for maintaining a leading edge in any sector. This dedication to continuous growth enables a company to remain flexible, responsive, and relevant in the face of evolving market needs and disruptive innovations.

Beyond strategic and operational goals, a company's core values, strong ethical standards, and a well-defined higher purpose are crucial. This is especially important in today's complex and often turbulent global environment. With rising social awareness, environmental concerns, and geopolitical tensions, stakeholders, encompassing employees, customers, investors, and the broader community, are now more focused not only on what companies do but also on how and why they do it.

Despite their current market dominance, tech giants such as Amazon, Microsoft, Google, and Facebook must continually evolve and improve their technology to maintain their position. Staying at the top is not automatic or without cost; significant investment in technological development and marketing is required to retain users.

While this may seem achievable for these companies, a deeper question arises regarding their underlying agendas and motivations. Can, or will, these conglomerates evolve spiritually and humanistically, or have they succumbed to an "ego trap" that provides a false sense of security? Their long-term survival might depend on their ability to adapt to a world of increasingly enlightened human beings.

History shows that competitors can, to some extent, surpass large organizations. Now, it is more important than ever for people to feel safe, secure, and protected from the violations that have become so common online. Evolution at every level is essential for survival in the digital world. Evolution is not static; it is a dynamic process.

Evolution or Revolution

Evolution in technology has accelerated into a profound revolution, resulting in a struggle between opposing forces. On one side, there is the potential for great good, driven by innovation that aims to uplift, connect, and address humanity's most urgent issues. This technology is born of humility, recognizing its role as a tool for improvement and shared progress. On the other side, the shadow of evil exists, where technological power is used for control, division, and self-interest, often fueled by unchecked ego and a desire for dominance.

In earlier times, simply possessing advanced technology might have been enough to assert power and maintain control. Military strength, industrial productivity, or sophisticated communication systems often determined global influence. However, today's world demands a much more subtle approach. The landscape has shifted significantly; information is everywhere, interconnectedness is a given, and the ethical implications of technological progress are increasingly scrutinized.

The dawn of the third millennium, in particular, marks a significant evolution of the human spirit. As our abilities proliferate, so must our sense of responsibility. This new era requires a fundamental change in what motivates those leading technological advancements. Future tech leaders can no longer be motivated solely by profit, market share, or personal gain. Instead, their choices and innovations must be based on truly altruistic motives.

This means focusing on the well-being of humanity, the sustainability of the planet, and the fair distribution of technological benefits. It involves a commitment to using power for the collective good, promoting collaboration over competition, and ensuring that technological progress benefits everyone, not just a select few. The ongoing struggle between good and evil, humility and ego, will ultimately influence the direction of this technological revolution and, in turn, the future of our civilization.

The current landscape of social, digital, and marketing platforms poses a significant challenge. Although they have established themselves as leaders worldwide, there is increasing concern that they are falling short in many areas. Several efforts have been made to create alternatives to the tech giants that currently dominate the online world. We are now witnessing a balkanization with many linear platforms and a rise of a parallel economy.

This raises essential questions about the future sustainability and adaptability of Big Tech. The core challenge lies in their ability to evolve. Can these monolithic platforms, built on centralized architectures and established business models, truly embrace and integrate emerging technologies? Or are they too entrenched in their existing structures to adopt disruptive innovations like decentralized blockchain?

Users often raise concerns about data privacy, algorithmic bias, inconsistencies in content moderation, and the widespread influence of advertising. From a creator's perspective, issues like revenue sharing, content ownership, and the lack of transparency in platform policies are common points of contention. For marketers, rising costs of acquisition, ad fraud, and restrictions on targeted advertising within walled gardens are increasing frustrations.

Decentralized blockchain technology introduces a fundamentally different approach. It offers increased transparency, greater user control over data, immutable records, and the possibility of new economic systems that could distribute value more fairly among participants. The challenge lies in whether current platforms can adapt to this decentralized future without jeopardizing their existing foundations. Currently, their business models rely heavily on data collection, centralized oversight, and proprietary algorithms – all of which contradict the core principles of blockchain.

The alternative scenario is that these platforms, despite their current dominance, may find themselves outmaneuvered by new entrants who are building natively on decentralized principles. Just as the internet disrupted traditional media, and social media disrupted early internet portals, a new wave of decentralized platforms could emerge that better address the evolving needs and expectations of users, creators, and businesses alike.

Ecosystems Are Evolutionary

Evolution is a natural and vital process, and this principle also applies to digital media. Just as the planet is a complete and interconnected ecosystem, we are now experiencing ecosystems within technology. This represents an evolution in itself and is necessary for a platform to be sustainable. Blockchain and cryptocurrency technology have enabled innovative companies and platforms to build systems from the ground up, addressing many of the controversial issues currently affecting social and digital media.

At the forefront of this digital revolution is Markethive, a pioneering and comprehensive ecosystem carefully designed to empower online users across many fields. Whether an individual explores the digital world mainly for social interaction, professional networking, inbound marketing, business ventures, artistic expression, or entrepreneurship, Markethive offers an unmatched platform.

It is based on the core idea that every person in their extensive network should be financially, professionally, and personally empowered, creating an environment where growth and self-fulfillment are natural results. This all-in-one approach makes Markethive unique, turning the traditional online experience into a dynamic and rewarding journey for all its members.

Markethive, the Social Market Broadcasting Network, stands out as a leading, ever-evolving platform. By utilizing blockchain technology, it has pioneered the first fully decentralized market network. This innovative approach offers a much-needed refuge from the internet chaos we have experienced, providing creative solutions and embodying humanitarian values that surpass those of older technologies and systems.

The Evolution of Decentralization

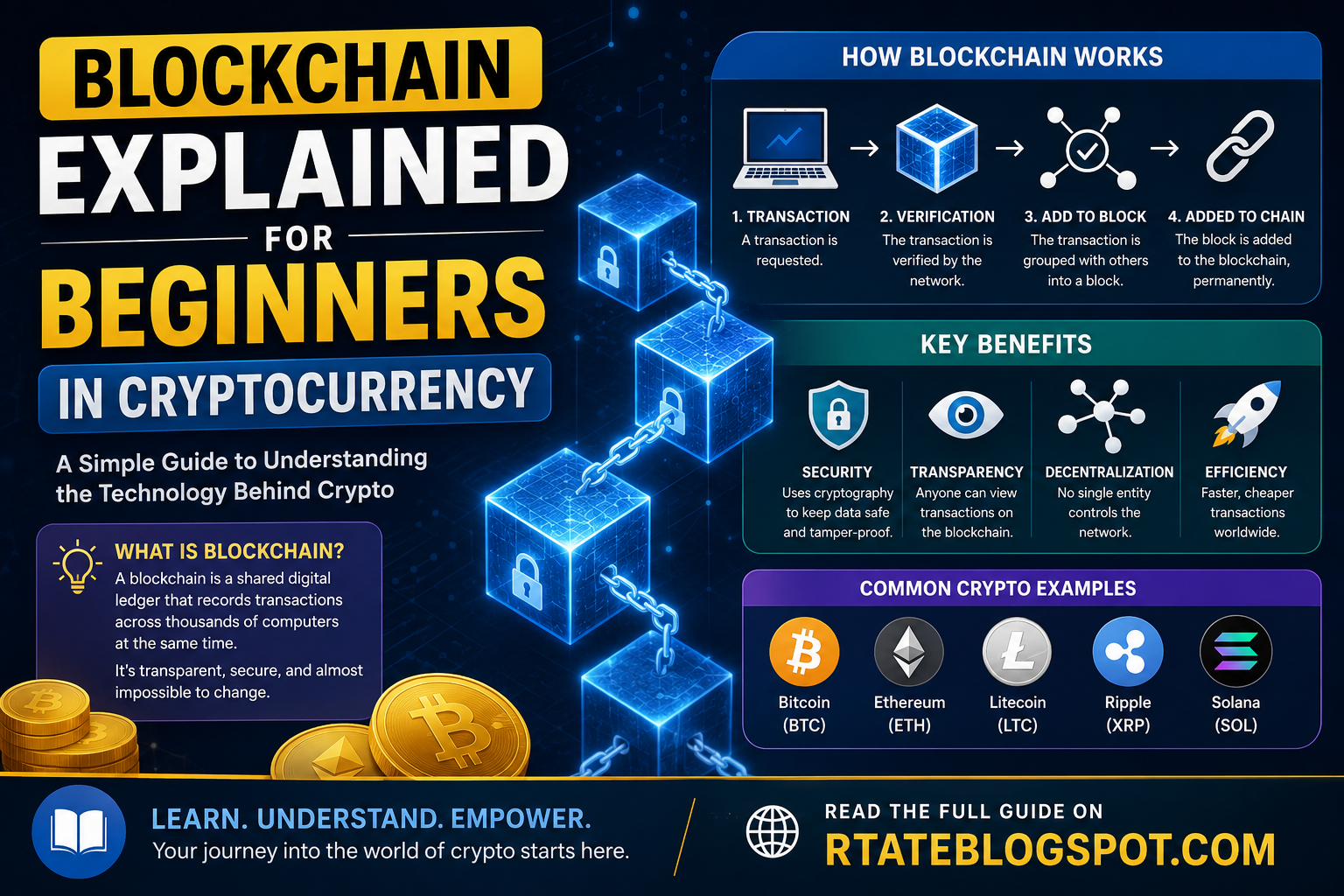

Blockchain is the Technology; Decentralization is the Movement.

Blockchain, at its core, is a revolutionary technology that enables the creation of distributed, immutable ledgers. It is a system of recording information in a way that makes it difficult or impossible to change, hack, or cheat the system. This technology underpins cryptocurrencies, but its applications extend far beyond digital money.

However, blockchain is more than just a technological innovation; it is the fundamental building block of a broader societal shift: decentralization. Decentralization is a movement that seeks to distribute power and control away from centralized authorities. In the context of blockchain, this means moving away from centralized entities, such as banks, governments, or large corporations, and towards a system where control is distributed among a network of participants.

The evolution of decentralization is key to understanding the long-term impact of blockchain. Initially, decentralization was about creating systems that could operate without a single point of failure. Over time, it has evolved to encompass concepts like transparency, censorship resistance, and actual ownership of digital assets. This ongoing evolution is crucial, as it addresses key concerns of trust, security, and fairness in the digital world. As the quality of decentralization improves, so too does the potential for blockchain to disrupt traditional industries and create entirely new paradigms for how we interact, transact, and govern ourselves.

.png)

The Evolutionary Imperative of Cryptocurrency

Cryptocurrency technology faces a critical juncture in its journey toward becoming a truly viable and pervasive alternative to traditional banking. Its future hinges on a continuous and accelerated evolution across several pivotal domains: scalability, transaction speed, security, and user accessibility.

- Scalability: Processing billions of transactions daily requires immense throughput, addressed by sharding, Layer-2 protocols, and new consensus mechanisms to rival global payment networks.

- Transaction Speed: Near-instantaneous transactions are crucial. This demands faster block confirmations and network optimization for quick, final validations.

- Security: Robust cryptographic protocols, resilient networks, and secure wallet technologies are paramount to prevent fraud and cyberattacks, building user trust.

- User Accessibility: Simplifying the complex user experience, including private keys, fees, and wallet options, is essential for mass adoption, aiming for ease of use comparable to credit cards or mobile payment apps.

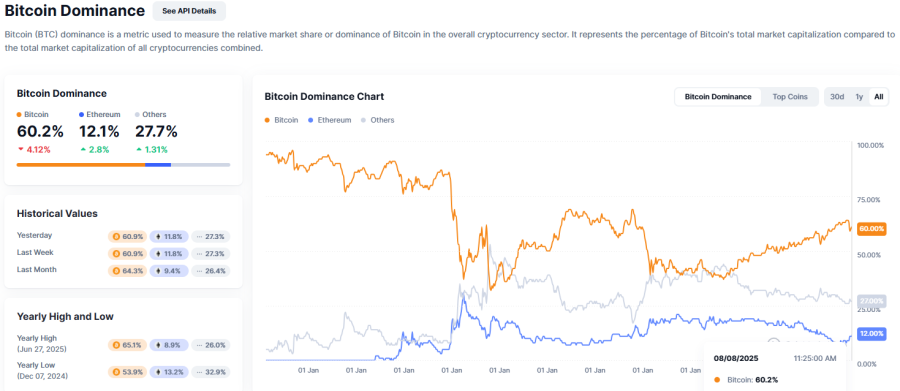

Over the last three years, both Bitcoin and Ethereum have undergone significant technological evolution, changes in market dynamics, and increased adoption. These developments have shaped their roles in the broader cryptocurrency ecosystem and influenced their respective trajectories, albeit on distinct yet complementary paths.

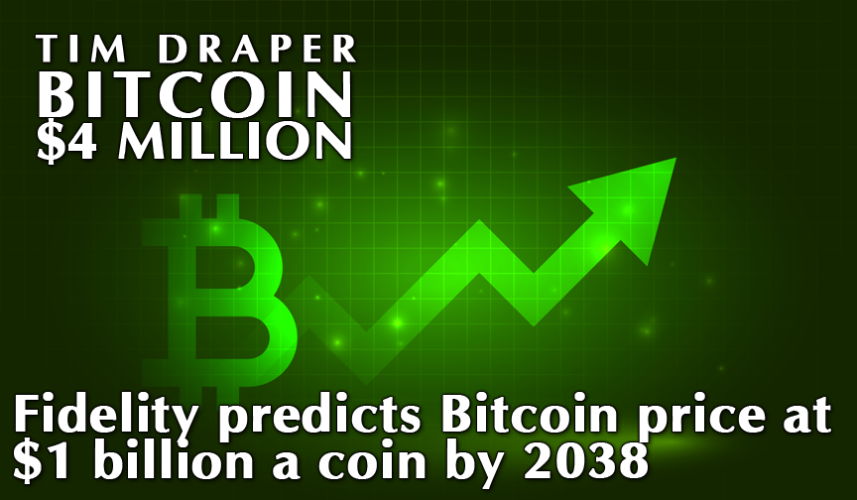

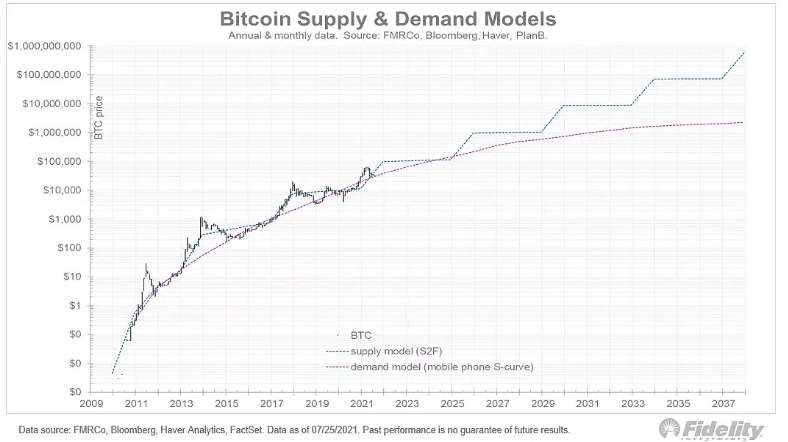

Bitcoin has evolved into a global financial asset, serving as a reliable store of value and inflation hedge due to several factors. Its digital scarcity, capped at 21 million coins, mirrors precious metals. The growing institutional adoption, including that of major financial institutions and nations, validates its potential for long-term growth.

Technological advancements, such as the Lightning Network, are improving scalability and transaction speeds, making it more practical for everyday use. Its deflationary nature, with a fixed supply and halving events, offers a strong hedge against inflation in an uncertain economic landscape. Ultimately, Bitcoin's increasing acceptance, innovation, and scarce design solidify its role as a fundamental part of diversified investment strategies.

Ethereum, since its creation, has undergone significant evolution, transforming into a strong and adaptable platform that leads the decentralized revolution. Its main strength is its ability to support decentralized applications (dApps) and self-executing smart contracts, which are key to a new era of digital interaction and finance. The platform's development has included several necessary upgrades aimed at overcoming its initial issues with scalability and sustainability. These improvements, such as the transition to Proof-of-Stake consensus with "The Merge," have significantly reduced its energy consumption and paved the way for future scaling solutions, including sharding.

Ethereum and other top cryptocurrencies continue to shape the future of digital finance. Their distinct features and diverse use cases are vital for promoting wider adoption of blockchain technology across various sectors. Ethereum, emphasizing programmability and supported by an active developer community, leads innovations in decentralized finance (DeFi), non-fungible tokens (NFTs), and Web3 applications. This ongoing progress, driven by increased institutional interest and clearer regulations, is steadily integrating blockchain into mainstream financial systems and everyday life, marking a significant transformation in how value is exchanged, stored, and managed globally.

Other notable cryptocurrencies include Solana, Cardano, and Elrond. All have made progress in their respective fields; however, their paths have diverged in terms of adoption and market performance.

Solana has quickly emerged as a leading force in scalable blockchain solutions, distinguishing itself through its innovative technological advancements and strategic partnerships. A key part of its rapid growth is its seamless integration with Bitcoin, which enhances interoperability and boosts the utility of both ecosystems. This integration not only enables cross-chain transactions but also leverages Bitcoin's proven security and liquidity, making Solana a more appealing platform for a broader range of decentralized applications.

Besides Bitcoin integration, Solana has a strong and expanding Decentralized Finance (DeFi) ecosystem with various protocols like DEXs, lending platforms, and stablecoins. Its fast transaction speeds, low fees, and innovative architecture (Proof-of-History and Proof-of-Stake) offer significant benefits for DeFi users and developers, ensuring efficient and affordable participation in the decentralized economy. The network's rapid growth in unique addresses and total value locked demonstrates its commitment to building a vibrant financial landscape, making Solana a leading player in blockchain and decentralized finance.

Cardano has consistently emphasized the development of its smart contract capabilities and the expansion of its decentralized application (dApp) ecosystem. Despite its robust research-driven approach and a dedicated community, it has struggled to achieve significant price momentum comparable to some of its rivals. This could be attributed to several factors, including the longer development cycles inherent in its peer-reviewed methodology and the challenge of attracting a broader developer base amidst stiff competition.

Elrond, now known as MultiversX, has a solid technical foundation with its highly scalable sharding system and adaptive state sharding. Although it is technologically advanced and offers impressive transaction speeds, it has not consistently attracted the same market attention or experienced the rapid growth seen in other blockchain projects. This could be due to a less aggressive marketing approach or the difficulty of standing out in a crowded, fast-changing blockchain environment, despite its innovative scalability and transaction processing methods.

Binance has undergone significant evolution over the past three years, marked by substantial growth in its services, strategic product expansions, and increased focus on compliance and user-centric offerings. The company has expanded its ecosystem to encompass a diverse range of financial products, including crypto payments, peer-to-peer (P2P) trading, and earning platforms. It has also made significant strides in the Web3 space, introducing features like Binance Square and enhancing its compliance and regulatory efforts.

The Elegance of Evolution

Technological evolution primarily showcases innovative ideas and creative visions rooted in a profound, often Divine, consciousness. This natural pursuit of progress is not random; it is a deliberate effort to significantly improve the current state of affairs. Its main aim is to elevate and enrich human life in all areas, covering basic needs and reaching for higher aspirations. This ongoing progress seeks to boost well-being, efficiency, connectivity, and understanding globally, continually pushing the boundaries of what can be achieved and shaping a future where human potential is fully realized.

Being the first to enter a market doesn't guarantee ongoing leadership or even the best choice. Sustainable success often belongs to strategic followers who learn from predecessors' mistakes, anticipate market changes, and provide refined solutions. Beyond strategy, a strong culture of goodwill, centered on ethical practices, fair dealings, and community engagement, builds trust and loyalty. Ultimately, successful companies blend strategic vision, ongoing learning, and a culture of goodwill, resulting in both financial gains and a positive societal impact.

As previously mentioned, this era emphasizes humanitarian and spiritual values. Unlike the industrial age, the focus is not just on business and profit but on the comprehensive and unified growth and well-being of the community as a whole. This involves looking beyond individual economic achievement to consider the broader effects on society. It includes not only financial success but also the emotional, social, and spiritual health of individuals and groups.

At its core, this era is devoted to spreading light, love, and peace. "Light" can be seen as a growth in knowledge, understanding, and transparency that dispels ignorance and fear, promoting a more enlightened perspective. "Love" urges greater compassion, empathy, and interconnectedness among all people. "Peace" involves actively resolving conflicts, fostering harmony, and creating environments where everyone can thrive. This shared aspiration for a more compassionate and enlightened world shapes the outlook for current and future generations.

Markethive and Markethive Media, an international company that represents everyone, will play a prominent role in the re-invention of the social media and marketing space to preserve and nurture the entrepreneurial spirit. It’s empowering the community by integrating Blockchain and cryptocurrency in a decentralized environment. Markethive has no agenda, and its heart and soul are freedom, liberty, financial sovereignty, and entrepreneurialism.

.png)

Editor in Chief Markethive:

Deb Williams. (Australia) I thrive on progress and champion freedom of speech. I embrace "Change" with a passion, and my purpose in life is to enlighten people to accept and move forward with enthusiasm. Find me at my

Markethive Profile Page | My

Twitter Account | and my

LinkedIn Profile.

Tim Moseley

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

%20copy(1).png)

.png)

.png)