Crazy Battle between Securities and Commodity Hangs Crypto in a Regulatory Limbo

Welcome to the fascinating world of cryptocurrencies, where digital assets have emerged as a disruptive force within the financial ecosystem. However, navigating the regulatory landscape surrounding these innovative forms of currency can be a bewildering experience. Despite their name, regulatory bodies like the Internal Revenue Service (IRS) do not recognize cryptocurrencies as currencies. Instead, they are often categorized as property, which has significant implications for taxation.

Simultaneously, the Securities and Exchange Commission (SEC) has raised concerns about initial coin offerings (ICOs) and their potential classification as securities. This has led to discussions around registration requirements and investor protections in the realm of cryptocurrencies. As a result, the emergence of cryptocurrencies has not only challenged traditional definitions and classifications of commodity and currency but has also blurred the lines between traditional financial instruments and these new digital assets.

Whether you are an investor looking to navigate the legal complexities of the crypto space or simply curious about the evolving nature of digital assets, this article aims to unravel the intricacies of the crypto landscape and shed light on how cryptocurrencies fit into existing regulatory frameworks. By exploring the classifications of cryptocurrencies as securities and commodities, we hope to provide you with a deeper understanding of their implications and the broader impact on the financial world.

Understanding Traditional Assets

To navigate the complex world of assets, it is essential to grasp the classifications established by regulatory agencies like the IRS, CFTC, and SEC for tax and regulatory purposes. While some definitions rely on legal precedents, such as the renowned Howey Test for securities, others may vary across regulatory bodies. Nonetheless, gaining a fundamental understanding of traditional assets is crucial before delving into the cryptocurrency spectrum.

There are three primary categories into which financial assets are typically grouped:

1. Real Estate:

Real estate, as a category of traditional assets, encompasses the land and any structures or improvements attached to it. This includes residential homes, commercial buildings, factories, warehouses, and even natural resources like minerals or water rights associated with the land. Real estate encompasses the tangible, physical properties and resources tied to a specific location.

When purchasing real property, certain fees and additional expenses contribute to the overall cost basis of the property. Specific rules and deductions apply to your taxes when dealing with real estate. By understanding the intricacies of real estate, including the costs involved in property transactions and the tax implications of property ownership, individuals can make informed decisions when buying, selling, or investing in real estate assets.

2. Securities:

Securities are financial instruments that represent ownership or a stake in a company or entity. They include familiar assets like stocks, bonds, and derivatives. The Securities and Exchange Commission (SEC) is the regulatory body overseeing securities in the United States. To shed some light on the legal aspect, in a significant court case called SEC v W. J. Howey Co. in 1946, U.S. securities law defined securities as "investment contracts."

In simple terms, when someone invests in a security, they expect to profit solely from the efforts of the issuer or a third party involved. These profits can come from selling the security at a higher price, receiving dividends, or earning interest. This landmark case established the "Howey test." It was utilized in various SEC enforcement cases, including disputes involving tokens like Ripple's XRP and the creators of NBA Top Shot, a digital marketplace for sports collectibles known as non-fungible tokens (NFTs).

3. Commodities:

Commodities refer to physical goods traded in large quantities on specialized exchanges. They can include agricultural products like corn and wheat and precious metals like gold and silver. Their current market price typically determines the value of commodities. The Commodity Futures Trading Commission (CFTC) oversees certain aspects of commodities trading in the United States.

However, it's important to note that the CFTC's regulatory authority primarily covers wrongdoing related to commodities futures trading rather than spot trading, which involves immediate transactions of physical goods. Spot trading of commodities doesn't fall under the CFTC's direct jurisdiction like securities do under the SEC.

As the popularity of crypto assets continues to soar, questions arise regarding how these conventional asset categories apply to the growing realm of digital assets.

Cryptocurrencies challenge the traditional notions of physical-focused assets, prompting regulators to adapt their frameworks and policies to encompass these innovative financial instruments. Consequently, exploring the distinct characteristics and implications of digital assets within the context of existing asset classifications becomes imperative.

Image source: Crypto.news

Why the Classification of Cryptocurrencies Matters

To truly grasp the different categories that crypto-assets fall into and how it impacts their regulation, it's essential to understand the meaning behind the Howey Test. The Howey Test has emerged as a widely respected method to classify these assets, and it does so by posing these fundamental questions:

1. Is money being invested?

2. Is there an expectation of earning a profit from the investment?

3. Does the investment involve a common enterprise?

4. Are profits generated through the efforts of others?

If a cryptocurrency meets all four criteria outlined in the Howey Test, it is considered a security. This means that promoters are actively marketing these tokens, while investors anticipate earning profits primarily through the efforts of others. SEC Chair Gary Gensler emphasized this point in a statement on September 8, emphasizing the prevalence of token sales where the public expects profits based on the actions of others. By understanding these criteria, individuals can gain insights into how crypto-assets are classified and regulated under the Howey Test.

If a cryptocurrency is classified as a security, it means that the issuers and exchanges of that cryptocurrency must obtain licenses from securities regulators. However, getting these licenses can be pretty challenging, which is why the crypto industry puts a lot of effort into ensuring that their cryptocurrency sales and projects comply with securities laws.

Issuers try to avoid violating securities regulations by focusing on decentralization. If a cryptocurrency is developed in a way that doesn't have a central group driving up its value, it becomes less likely to be seen as security by regulators. This is why decentralized finance (DeFi) projects work towards decentralizing their development efforts and splitting governance through decentralized autonomous organizations (DAOs).

They also utilize mechanisms like proof-of-stake as a consensus mechanism. The argument behind this approach is that if people are both investors and actively participate in the project's growth, such as by staking the coin or voting in DAO decisions, they are no longer solely reliant on a third party to generate returns, as required by the Howey test.

The risk of classifying cryptocurrencies as securities is that exchanges may choose not to list them to avoid being fined by the Securities and Exchange Commission (SEC) for trading unregistered securities. Cryptocurrencies may face state-specific rules and regulations. For instance, the New York Attorney General filed a lawsuit against KuCoin, and multiple state regulators have teamed up to target a coin featuring Elon Musk's image called TruthGPT Coin. These cases highlight the potential legal complications that can arise.

The SEC has provided guidance on initial coin offerings (ICOs) and digital assets. In their framework for the investment contract analysis of digital assets, the SEC emphasized factors such as the speculative nature of many ICOs and their lack of utility as payment or store of value, which could lead to these coins being classified as securities. Kik, an ICO project, faced legal consequences when its CEO said buying its tokens would result in significant profits. The SEC sued Kik, and the company was fined $5 million, nearly pushing them to bankruptcy.

Conversely, the Commodity Futures Trading Commission (CFTC) argues that cryptocurrencies like Bitcoin and Ether are commodities and can be regulated under the Commodity Exchange Act (CEA). The CFTC's rationale is based on the fact that cryptocurrencies like Bitcoin are interchangeable on exchanges, just like sacks of corn of the same grade have the same value. This determination was reinforced in the CFTC's case against Bitfinex, a crypto exchange, and Tether, a stablecoin issuer, where the agency stated that digital assets like Bitcoin, Ether, Litecoin, and Tether are all commodities.

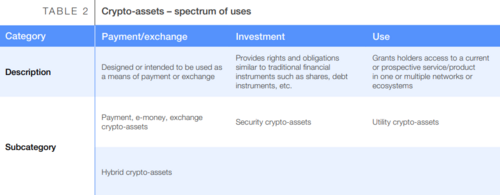

Determining whether cryptocurrencies fall under the classification of securities or commodities has significant implications for their regulation. It affects licensing requirements, listing on exchanges, compliance with securities laws, and potential legal consequences. These classifications shape the regulatory landscape and play a vital role in how cryptocurrencies are treated within the financial ecosystem.

Image credit: Markethive.com

Where Things Stand in The Ongoing Regulatory Debate

The regulatory landscape for cryptocurrencies is constantly evolving, and it's challenging to predict how it will look in the future. Various stakeholders and factors are involved, making it a complex situation. In the United States, Congress has made efforts to grant the Commodity Futures Trading Commission (CFTC) broader authority to regulate the spot trading of non-securities tokens. Among these tokens, Bitcoin is currently the only one that both agencies, the CFTC and the Securities and Exchange Commission (SEC), openly agree on its classification.

One possible outcome of this ongoing debate is that specific cryptocurrencies may be classified as securities while others are treated as commodities. This would create an even more intricate regulatory landscape where different cryptocurrencies are subject to different rules and regulations.

Alternatively, lawmakers could establish crypto as its distinct asset class, introducing tailored regulations specifically for cryptocurrencies. This approach is largely followed by the European Union, which has implemented the Markets in Crypto Assets (MiCA) regulation. MiCA outlines steps that crypto issuers, wallet providers, and exchanges must follow to protect consumers and ensure fair trading.

However, even with these regulations in place, there may still be some legal areas that need to be addressed on a case-by-case basis. For example, determining whether a particular series of non-fungible tokens (NFTs) must adhere to specific rules. As the discussions continue and regulatory bodies navigate the complexities of cryptocurrencies, it remains a dynamic and evolving landscape with ongoing developments that will shape the future of crypto regulation.

Controversial Guidelines on How Cryptocurrencies Are Classified

The classification of cryptocurrencies has been a contentious issue, with different U.S. regulatory agencies offering their own definitions. The Securities and Exchange Commission (SEC) labeled cryptocurrencies as securities, considering them investment assets that generate returns. This categorization was based on federal security laws and the belief that anything traded on an exchange qualifies as a security, including cryptocurrencies.

However, the Commodity Futures Trading Commission (CFTC) took a different approach. Following a court ruling.pdf, the CFTC gained the authority to regulate digital currencies as commodities, treating them similarly to products like coffee and oil.

Additionally, the Internal Revenue Service (IRS) defined cryptocurrencies as taxable property for federal tax purposes, adding another layer to the classification debate.

Two other agencies, the Office of Foreign Assets Control (OFAC) and the Financial Crimes Enforcement Network (FinCEN), also provided their guidelines. OFAC considered digital currency on par with fiat currency, while FinCEN categorized cryptocurrencies as a form of money. These distinctions diverged from other agencies' commodities, property, or asset classifications.

These conflicting definitions within the same government highlight the challenge businesses face in legally classifying cryptocurrencies. However, efforts have been made to bring more clarity. For example, the SEC clarified that it does not consider Ethereum and Bitcoin securities but focuses on Initial Coin Offerings (ICOs). While there is an ongoing debate, this statement narrows the understanding of cryptocurrencies within the United States.

The different classifications can create confusion for businesses, which may struggle to understand which regulations apply to them. This confusion can lead to legal risks if companies fail to comply with the appropriate regulations. It can also discourage some businesses from entering the cryptocurrency market due to the uncertainty and complexity of regulations.

Moreover, the classification can impact innovation in the crypto industry. If a new cryptocurrency is classified as a security, it may deter innovation due to the stringent regulatory requirements. Conversely, if classified as a commodity, it may encourage development due to the relatively less strict regulations.

However, it's important to remember that the regulatory landscape for cryptocurrencies is still evolving, and changes may occur in the future that could affect crypto businesses. Therefore, it's crucial for companies to stay updated on the latest regulatory developments and seek legal advice to ensure compliance.

Classifying cryptocurrencies as securities or commodities is complex, with significant implications for investors and regulators. As the cryptocurrency market continues to evolve, it may be necessary to reevaluate and refine these classifications to reflect this asset class's unique nature accurately.

While the current classifications provide some clarity, they also highlight the need for a more nuanced regulatory framework to accommodate cryptocurrencies' distinctive characteristics. This is a challenge that regulators worldwide will need to address in the years to come.

This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

.png)

Tim Moseley

.png)

.png)

.png)

(28).gif)

%20copy.png)

.png)

.png)

.png)

.png)

.png)

.png)

(27).gif)

.png)

.png)